I spend 3 hours on a daily basis to commute to & from work. When you live in Mumbai, you learn how to hustle. It gets embedded in your DNA.

What you learn, is how to save the most valuable [and the most scarce] resource in the world. TIME.

Every second counts.

To save time, I started buying Metro tickets on Paytm. You get the QR code on the app. You can easily scan it at the entry gates. Saves paper. Saves time. Its a win-win. And, its a sticky product.

If you analyze the Paytm mobile app, you’ll see that you can practically do anything on the app.

You can pay your utility bills. You can take a personal loan & apply for a credit card. You can book tickets for any mode of transport (air/train/bus/metro). You can book movie tickets. You can even trade & invest through Paytm!

If you’ve got a good product, you should be running a decent business. So, why is the stock price of One 97 Communications (the parent of Paytm) falling?

The most important question:

Is the current stock price a good entry point for investors?

Let’s find out.

Where are the profits?

If you read the 20 page Q1FY23 earnings report of Paytm, you will notice the word ‘profit’ is being used a LOT of times. Vijay Shekhar Sharma, has promised that Paytm would become operationally profitable at an adjusted EBIDTA1 level by September 2023.

Can it achieve this aggressive target?

Before we answer this question, let’s understand how Paytm makes money.

Paytm has 3 SOURCES of income:

Payment Services - this is the commission that Paytm earns from its users on select transactions & from merchants that use the Paytm app for business. Merchants also pay subscription fees for payment devices. Paytm recovers UPI incentives from the Government, since UPI is free & Paytm recovers the cost of maintaining the UPI2 infrastructure from the GoI.

Financial Services & Others - Paytm has partnered with Banks/NBFCs to disburse loans through its platform to its users & merchants. Paytm charges a sourcing fee & collection fee from its loan partners for every loan disbursed. It charges upfront distribution fees for credit cards issued & a % of total credit card spend. It also earns from insurance commission & equity brokerage.

Commerce & Cloud Services to Merchants - Paytm makes money through enabling commercial activities for its merchants like (i) advertising (ii) tickets sales related to travel & entertainment (iii) deals/vouchers

What’s holding Paytm back?

Net profits.

The company has accumulated losses of INR 13,200 Crore. It reported a Q1FY23 loss of INR 644 crore despite a 88% increase in revenues. Employee costs & marketing costs remains high. It is spending a lot of money on cash backs. ESOP costs are so high that the Company is computing its profitability excluding ESOP costs. [which doesn’t make sense to me]

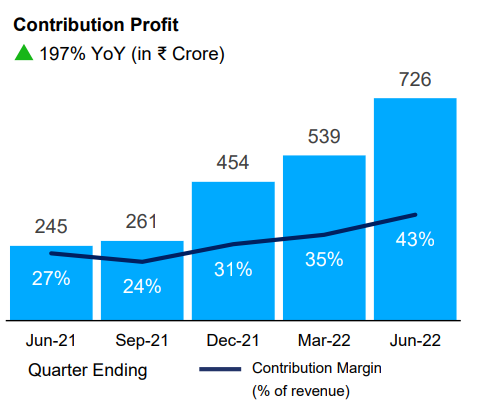

There are some positives from the Q1 earnings report. The contribution of financial services (which is a high margin segment) in the total revenue is increasing.

Number of payment devices deployed by merchants increased YoY, the number of merchants on the platform also increased YoY. Paytm’s customer acquisition cost remains low & there is a lot of scope for cross selling and monetizing its wide range of products & services.

Its net payments margin increased to 35% and gross margins increased to 43.2%.

Should you buy Paytm?

The metrics above show that Paytm is slowly inching towards profitability. Vijay Shekhar Sharma, the Company’s CEO is confident that they will achieve profitability (excluding ESOP costs) by September 2023.

I think that’s an aggressive target, since payment services still remains the Company’s core business. Competition in the payments space is intense with players like Google Pay & PhonePe.

Financial services & loan disbursements are growing at an incredible pace, but fintech remains a sector under the lens of RBI and increased regulations could pose risks for Paytm.

The stock is trading at INR 638, down by > 70% from its issue price of INR 2150. However, its market capitalization is still > 41,000 crore.

Which means, all future profits discounted should be > 41,000 crore (theoretically)

The next few quarters would be important, because unless the Company starts churning out a profit (after considering ESOP costs), the stock would look expensive perpetually even at INR 638.

(Disclaimer: The author of this article is not an investment advisor or a certified wealth manager. The readers are advised to do their own research before deploying their capital into financial securities.)

Adjusted EBITDA is computed after excluding ESOP costs.

UPI incentives were not booked as revenues for Q1FY23.