What is the reason behind the rise of MTAR Technologies?

why has the stock delivered 3X returns in the last one year?

My last update on MTAR Technologies was 2 years back where I had highlighted several issues.

First concern was management revising its estimates every quarter and the delta between the estimates and actual revenue. Take a look at the summary below:

Evolution of FY24 forecast — INR 860 Cr → INR 700 Cr → INR 610 Cr → INR 580 Cr [actual FY24 revenue]

Evolution of FY25 forecast — INR 900 Cr → INR 676 [actual FY25 revenue]

FY26 guidance — INR 900 Cr → achieved INR 571 Cr upto 31st December [9 months] + needs to achieve INR 329 Cr in Q4FY26 [low probability]

FY27 guidance — INR 1,350 Cr → guiding 50% growth YoY [I would take this # with a pinch of salt]

When management consistently misses their estimates, it tells you plenty of things. One, that the business might have lumpy revenues. Two, the management doesn’t have a strong grip on execution. Three, management over-promises and under-delivers. Things that don’t instill a lot of investor confidence.

Few other concerns were the high working capital nature of the business and customer concentration [reliance on Bloom Energy].

What’s baffling, is that despite the miss in estimates — the stock price has continued to ZOOM higher and the stock is trading at a P/E of 172 times. There’s a strong reason for this surge, and the markets feel that MTAR could significantly scale in the future.

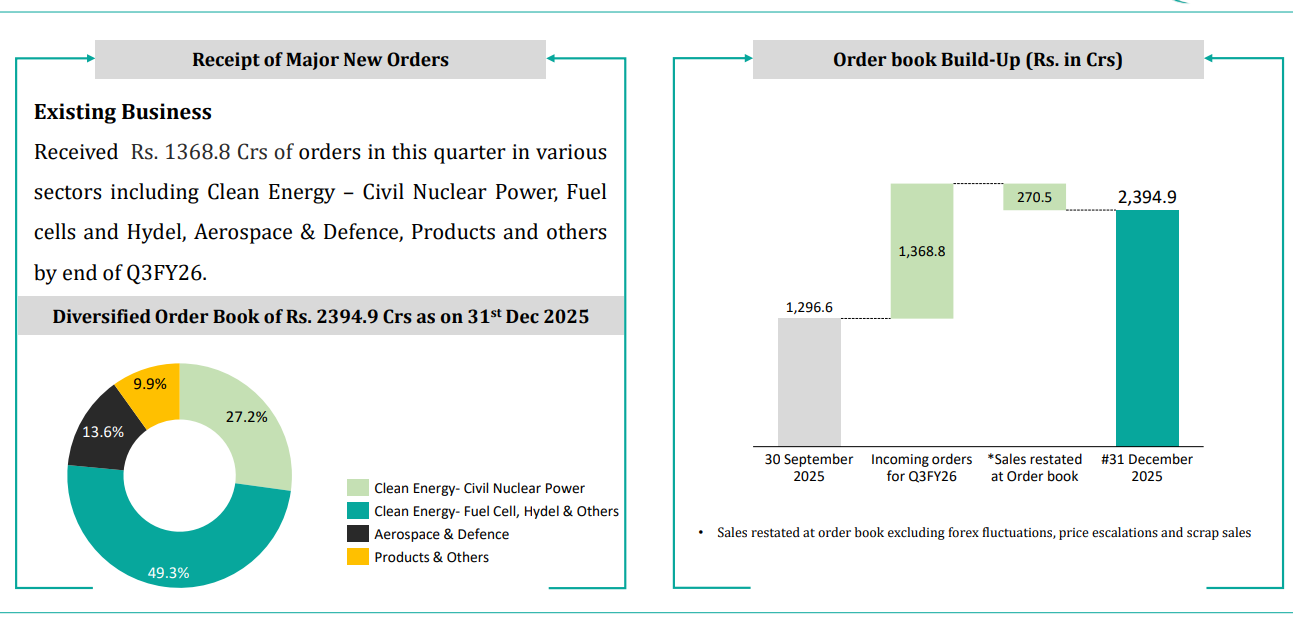

Growing Order Book

As at 31st December 2025 — MTAR had an order book of INR 2,395 Cr and the management is expecting to close the order book at INR 2,800 Cr [3.5x FY25 revenues]

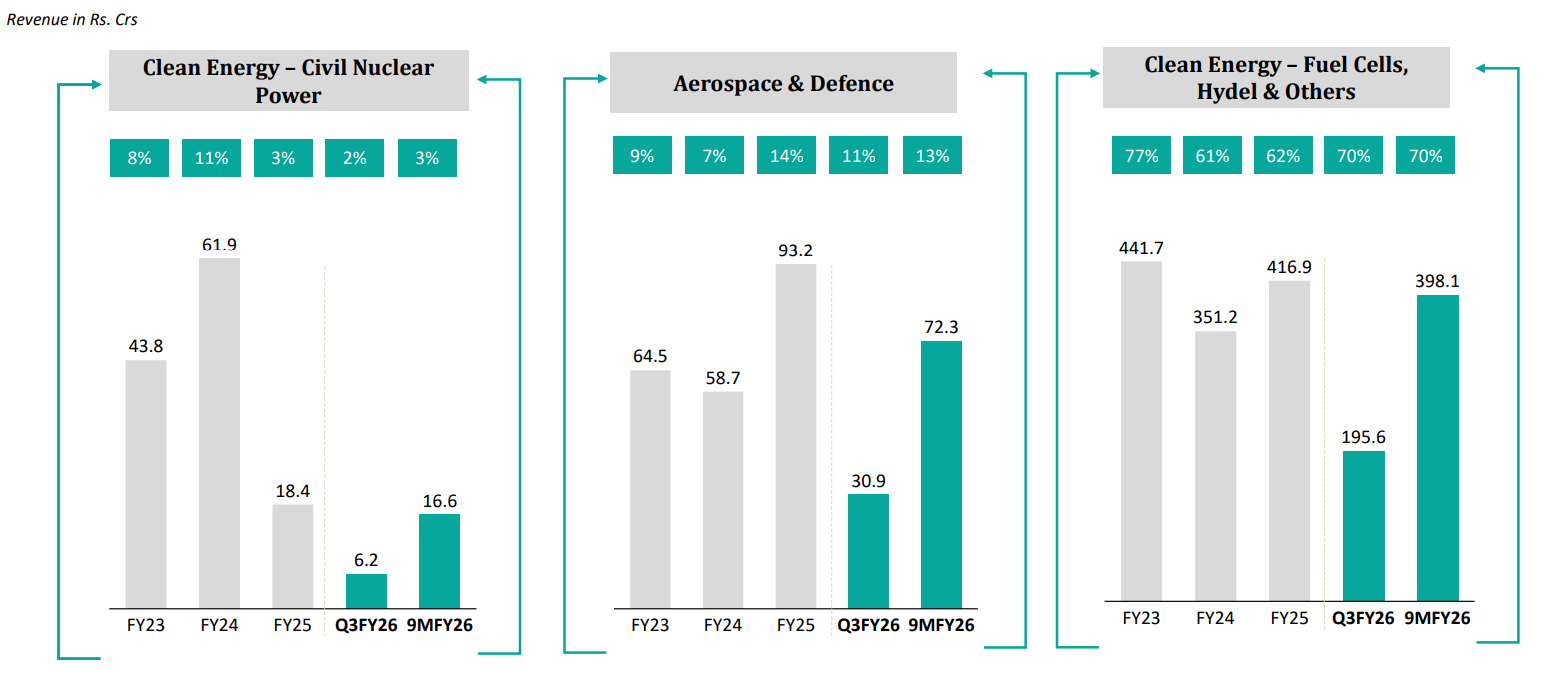

Clean Energy Fuel Cells

70% of total revenues come from this segment. The company makes various products like hot box assemblies, hydrogen boxes, electrolyzers & sheet metal assemblies. Most of the revenue from this segment comes from a single customer — Bloom Energy.

A hot box is the heart of a fuel cell where the electro-chemical reaction occurs to generate electricity. MTAR is the sole supplier of these hot box assemblies to Bloom Energy.

Bloom Energy is witnessing a strong growth for its solid oxide fuel cells [SOFC units], due to a rise in demand for AI data centres — which are extremely power hungry. The world is looking for clean [and sustainable] sources of energy, hence driving strong adoption of SOFC units.

Bloom Energy entered into a $2.65 billion agreement with AEP for supply of SOFC units. The company is expected to grow at a CAGR of 30% upto FY30 + is investing in additional SOFC capacity.

As Bloom grows, so will MTAR — since it is intricately connected to Bloom Energy’s supply chain. Subsequently, MTAR is increasing it’s manufacturing capacity for hot boxes from 8,000 [current] → 12,000 [by end of FY26] → 20,000 [end of FY27] → 30,000 [end of FY28].

Probably why the stock price popped.

The company would incur a capex of INR 100 Cr to achieve this by FY28 — which isn’t a BIG number. What this means is that the company can scale without incurring significant capex. A very positive sign.

Apart from Bloom Energy, MTAR is working with several other customers — GE, Andritz & Voith and recently finalized a deal to supply INR 40 Cr of orders every year to Andritz. A small step in customer diversification.

Nuclear Energy

India is making moves in the nuclear sector — with the Government opening up this sector for private players + evaluating a INR 20,000 CRORE PLI scheme for manufacturing critical nuclear components.

India has a target of achieving 100 GW of nuclear power capacity by 2047 [quite ambitious], with a planned expansion of small modular reactors.

MTAR has received orders worth INR 500 Cr+ for Kaiga 5 & 6 reactors [in Karnataka] and is expecting to play a key role in establishing nuclear reactors by supplying key assemblies.

Currently, revenues from this segment are only 3% of topline. Going forward, with a flux of orders, this mix should change.

MTAR makes critical fuel handling equipment for the core of nuclear reactors — fueling machine heads, coolant channel assemblies, fuel transfer systems etc. The company has been in this business of 40+ years, with close relationship with NPCIL. And the barriers to entry in this business are quite high.

Management expects INR 300 - 500 Cr of orders every year, with order potential of INR 350-400 per reactor. Expects a lot of reactors coming online in the next 5-10 years. Just what the investors want to hear.

Aerospace & Defence

Focusing on next generation technologies and structural assembly orders. The company is working on several prototypes & first articles and is expecting to enter volume production in the future.

Revenue estimate of INR 150-160 Cr [FY27] → INR 350-400 Cr [FY29]

I think the revenue estimates are quite aggressive and it remains to be seen how prototypes convert into production orders.

Concerns

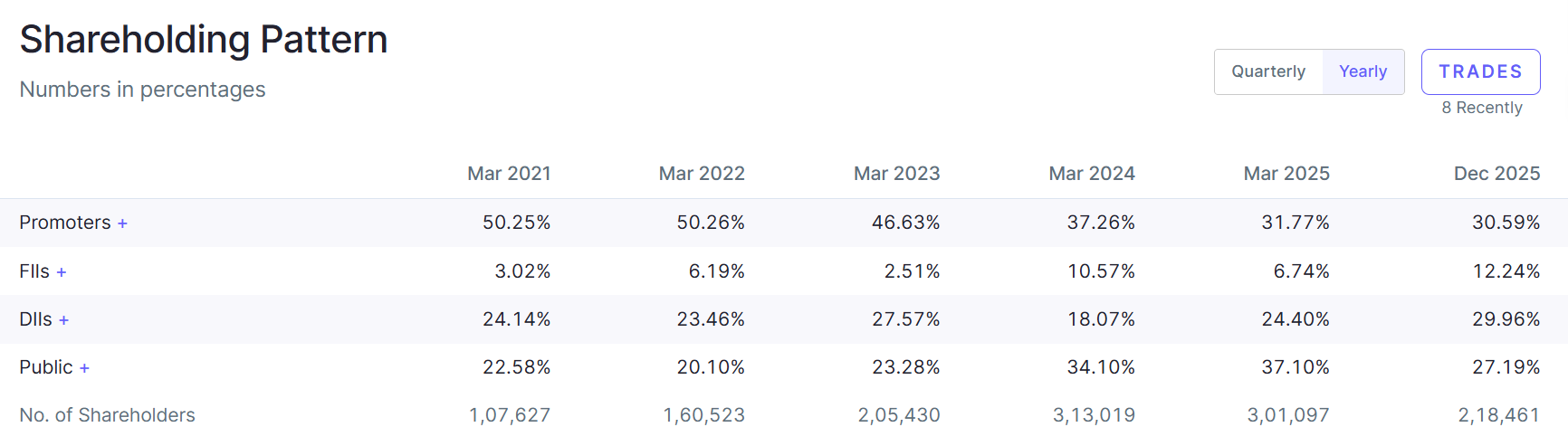

One major concern is decline in promoter shareholding over the years. The management has termed this an exit of non-core family members — however I don’t buy it. Why would you sell a stock IF you know that a company is going to do well in the future?

Some selling is okay, since the stock price has skyrocketed in the last one year. Promoters are human beings and they are permitted to book profits. However, consistent decrease in promoter shareholding could mean deeper structural issues.

9% of the promoter shareholding is pledged, which could lead to selling pressure in case the stock tanks substantially.

High participation from DIIs / FIIs means the stock has become mainstream, hence the high valuation. Once mutual funds buy into a stock, monthly SIPs of retail investor starts flowing into the stock, leaving little opportunity for generating out-sized returns.

Conclusion

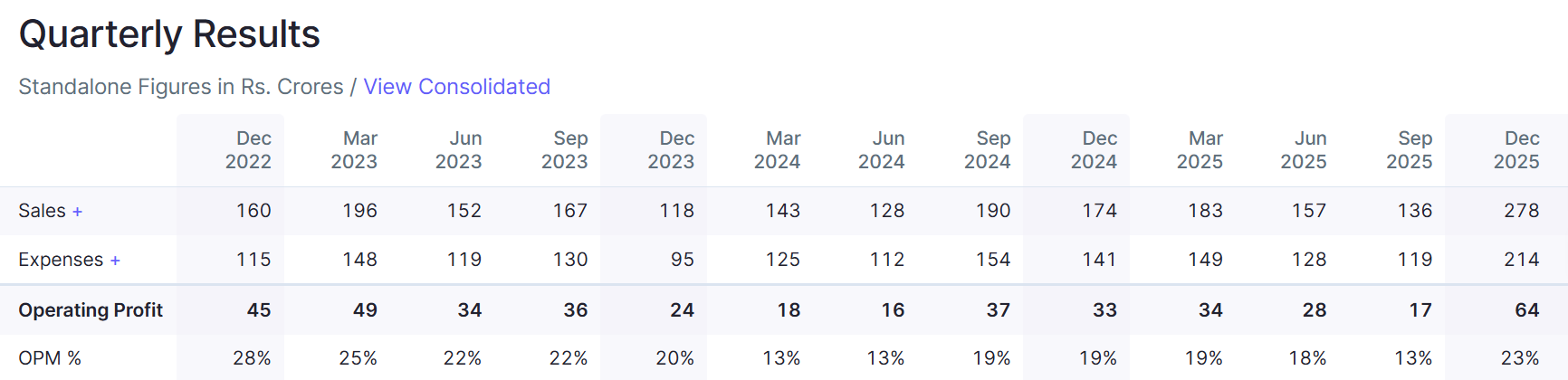

Q3FY26 was a really good quarter for the company — with revenue UP 60% YoY. Operating profits UP 88% YoY. Margins expanded from 19% → 23%, due to operating leverage.

The demand surge for fuel cell hot boxes from Bloom Energy + uptick in orders pertaining to nuclear reactors — could lead to significant future growth for MTAR. I’d like to see if margins can further expand from here.

Management has guided for FY26 EBITDA of 21% — and is expecting margins to rise as orders get realised from nuclear & aerospace segments [which have higher margins]

Execution risks remain, as the management has consistently missed estimates. At a P/E of 172 times, the current valuation doesn’t offer a lot of upside. Although, the company is doing some interesting things, and deserves to be tracked closely ;)

If you liked this article, share it in your investing network. Comment, like, show some love! I spend a lot of time in research & it would mean the world to me if you could recommend this blog to your friends.

[Note: The author is not a SEBI registered investment advisor and the contents of this article do NOT constitute investment advice. Always do your own research before you invest in a company]