#QuarterlyUpdates : DreamFolks Q3FY24

Airport lounges used to be exclusive. You’d see business travelers with their laptops and you’d strive to be a part of that exclusive club. That is a thing of the past now, because with more credit card penetration offering lounge access — people have started to line up to get in an airport lounge.

With low cost carriers not offering food, people have started utilizing the complimentary food offered at airport lounges.

DreamFolks Services Limited — is in the business of airport services and derives majority of it’s income from airport lounge aggregation.

ALSO READ: Detailed breakdown of DreamFolks’ business model in this article

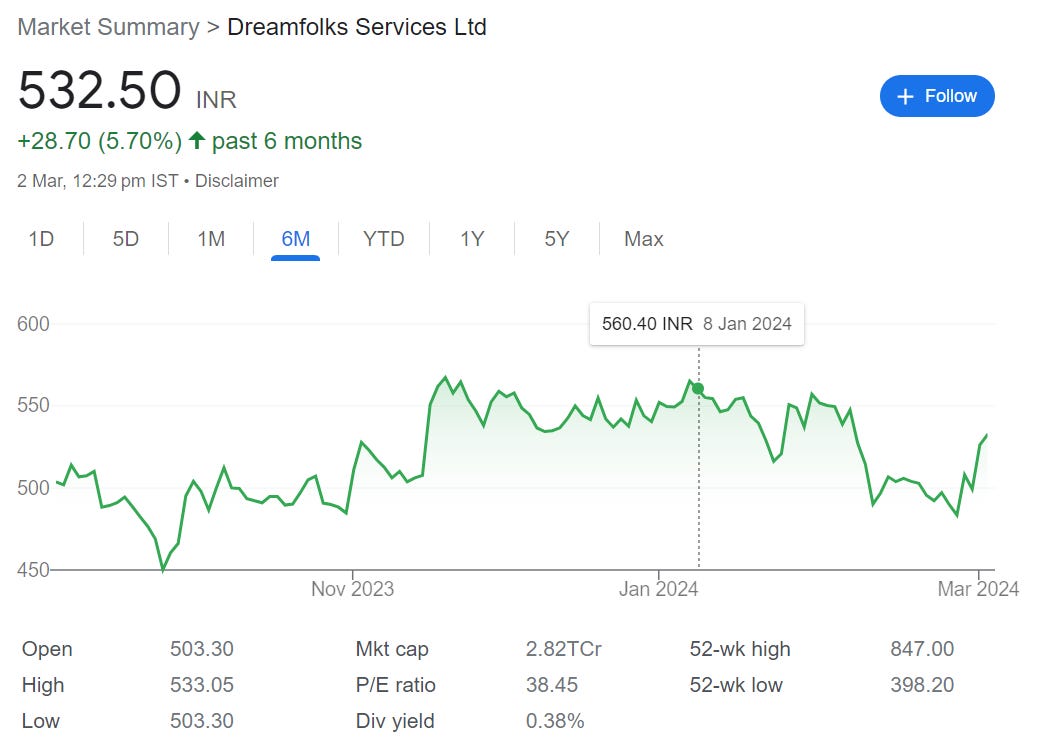

The stock price has been flat for the past 6 months — and at a PE of 38 times the stock looks a little expensive, given that expanding margins might not be easy for the company.

With that, let’s take a look at the Q3 performance!

Q3 Performance

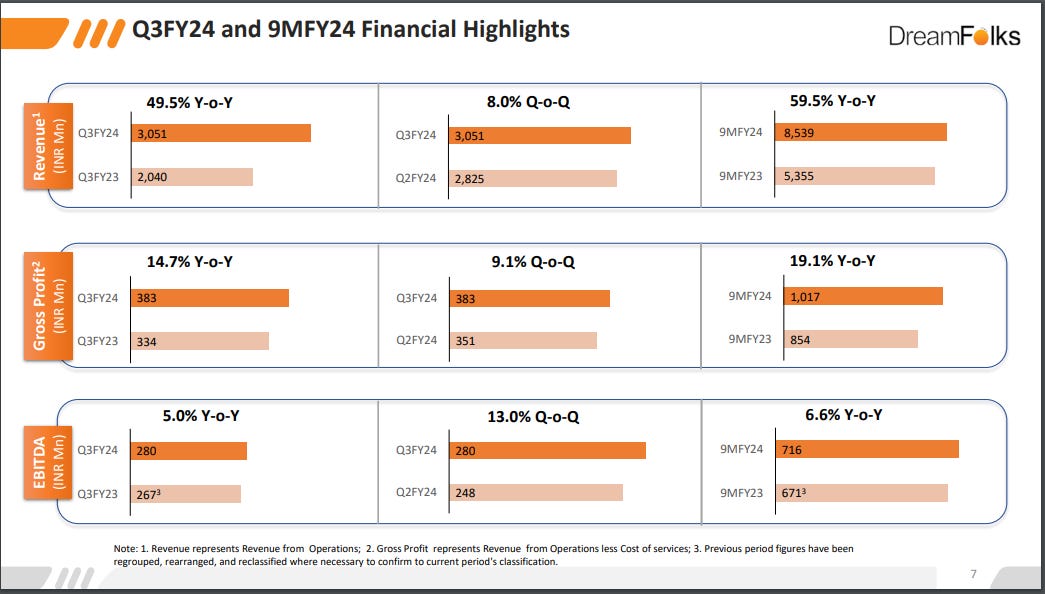

The company had a decent Q3 performance in absolute terms. Revenue was up 50% YoY. Gross Profit was up 15% YoY and EBITDA was up 5% YoY.

However, if you look at the margin percentages — they have fallen YoY.

Gross profit margin has contracted from 16% in Q3FY23 to 12.5% in Q3FY24

EBITDA margin has contracted from 13% in Q3FY23 to 9% in Q3FY24

Management expects gross margins to be in the range of 11%-13% for the next few years.

So, in absolute terms the Q3 performance was good. But you can see erosion of margins YoY which is concerning if you’re an investor because this signifies that the company doesn’t have a lot of pricing power.

I spoke about this in length in my original article — speaking about a BIG RISK in the business model of DreamFolks.

Key highlights for the quarter:

DreamFolks launched their exclusive membership program — ‘The DreamFolks Club’ which bundles various services into a package. There are 4 package variants with pricing ranging from INR 6,999 to INR 99,999.

The idea is to cater to that class of customers who don’t have debit cards / credit cards but still want to avail such services.

Primary target audience of this membership program are enterprises / MNCs who want to provide rewards to their employees / channel partners / customers etc.

How BIG of an opportunity could this be? Management did not provide specific commentary on this and we would have to see the next few quarterly updates to see how this plays out.

Partnered with Grey Wall — Russia’s leading lounge operator. Through this partnership Indian passengers can gain access to around 100 lounges located in key airports + railway stations in Russia. Alternatively, Russian passengers will gain access to lounges in India.

The company expanded their presence in railway lounges in Chennai and Old Delhi and continues to maintain a 100% coverage in railway lounges across India.

Added two new services where it will act as an aggregator:

Pathology testing across India — through a strategic partnership with Healthians.

Gifting services allowing customers to send flowers, cakes, planters to friends / family through partnership with My Flower Tree.

Growth drivers for the business will be increase in credit card penetration + increase in airport traffic.

India’s credit card penetration is as low as 5.5% — growing from 7.5 crore credit cards in April 2022 to 8.6 crore credit cards in April 2023. This number is expected to grow to 10 crore by April 2024.

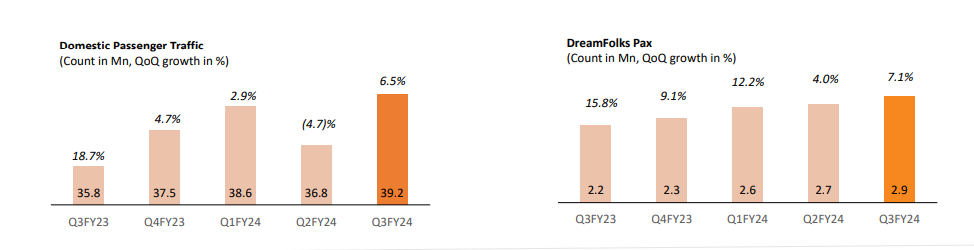

In Q3, air passenger traffic grew by 9% YoY to 39 million passengers as per DGCA data. Air traffic is expected to grow in India for the foreseeable future.

Data on passenger traffic for Q3

Some concern points to note:

Credit card companies are shifting from the current ‘fixed benefits’ model to ‘spend based’ model — meaning that if you hold a credit card, you will NOT be getting lounge benefits by default anymore. You will have to spend a certain amount of money through the card, to unlock lounge access.

This would result in lower volumes for DreamFolks because not everyone holding a credit card will be able to spend enough to unlock lounge access.

Although not all credit card companies have shifted to the spend based model — and management has seen customers shift to alternative credit cards which are still offering fixed benefits.

However, sooner or later — this is the trend that all credit card companies will follow and this will impact DreamFolks’ business in an adverse way.

DreamFolks has launched various services like e-SIM, VISA services, Spa, Golf services, airport dining etc. — however these services have a negligible contribution to the topline (around 1-2%).

Management expects these services to contribute around 20% to the topline in the next 4-5 years — but I think that is extremely conservative and the management should push to generate more revenues from these initiatives to de-risk from airport lounge access which contributes 97-98% of the total topline.

These services would command a higher margin compared to airport lounge access.

Employee benefit expenses have increased due to increase in ESOP expenses — which forms around 20% of total employee costs, which looks quite high.

Q4 is expected to be flat in terms of revenue, since Q3 was a seasonally favorable quarter. The business thus, has a touch of cyclicality to it.

Conclusion

DreamFolks has a 95% market share of the card based lounge access in India. It had a decent quarter with reasonable growth in topline.

I am looking forward to see how the traction builds up in it’s exclusive membership program — wherein it will not be dependent on credit card companies to pay them.

This looks like a program, wherein DreamFolks could command some sort of pricing power — but will it be a profitable venture? Can it lead to margin expansion in the long term?

That is the question that investors should concern themselves with.

In the current business, it doesn’t have a lot of pricing power — with gross margins being range bound between 11-13%. Other services will start contribution to profits only after 4-5 years.

Credit cards shifting to a spend based model will also impact volumes — however management doesn’t expect a significant adverse impact due to this change.

They’ve already captured the major share of the market, so the only way to grow is increase in credit card penetration + adding more lounges to it’s network + more air passenger traffic.

At a PE of 38 times at a market capitalization of 2,700 crore [as at 04 March 2024] — I would say the company is a little expensive. Not the best price point to enter the stock, but you could track it. And as always, I will keep bringing quarterly updates to your attention :)

If you liked this article, share it in your investing network. Comment, like, show some love! I spend a lot of time in research & it would mean the world to me if you could recommend this blog to your friends as well OR you could contribute by donating a small token to fund my research!

[Note: The author is not a SEBI registered investment advisor and the contents of this article do NOT constitute investment advice. Always do your own research before you invest in a company]