6 months back, I had written a detailed article on Avalon Technologies — a company in the business of electronics manufacturing [EMS].

India — although late to the party — is serious about building EMS capabilities and is investing in various programs like the PLI schemes, Electronics Component Manufacturing Scheme [ECMS], India Semiconductor Mission 2.0 [ISM 2.0] etc.

The intent is clear — India wants to be a reliable partner for any global counterpart looking to de-risk their supply chain away from China. India cannot completely replace China [that might take decades] but can slowly chip away at the global EMS market share.

Verdict?

Increased business for Indian EMS players, and because it is not a zero-sum game, multiple companies can win and co-exist — because the pie keeps getting bigger.

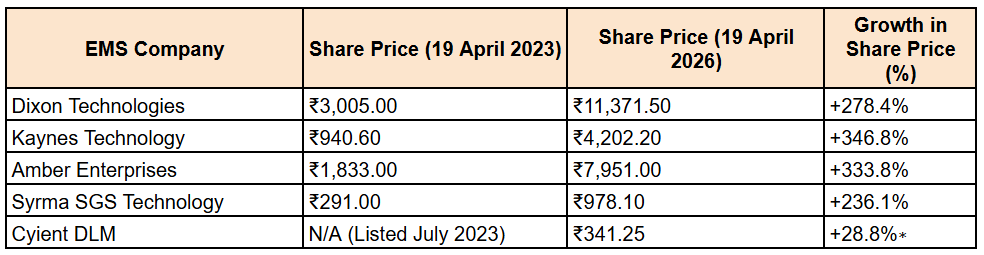

From the table above, you can see that some of the key Indian EMS players have been on a tear for the last few years delivering stellar returns to investors. Can this run continue? Which stock would be the best pick? Should you follow a basket approach — investing equally in 5-7 EMS players?

Unfortunately, no one knows. However, one thing is clear — that this sector deserves your attention. The potential for growth is immense and what we can do is learn about the players and place our bets accordingly.

Avalon Technologies - a quick brief

If you’re lazy to read my original article on Avalon, here’s a quick summary of how they make money.

Avalon was incorporated in 1999, headquartered in Chennai. It started with the business of PCB assembly, got into magnetics → plastics → metal assembly → cable assembly → wire harnesses → and ultimately became a fully integrated EMS player delivering box-build solutions.

The business model is simple — customers want electronic components but don’t want to build their own manufacturing facilities, so they sub-contract the process to companies like Avalon. And for the manufacturing process, customers pay a service fee.

Avalon has 15 manufacturing facilities — out of which 2 are based in the US, giving it a unique leverage over EMS players who only manufacture in India.

The switching costs in the EMS business are quite high — meaning that once you win a customer [which takes a considerable time], the customers stick with you for a long time. Unless you screw up big time.

The reason is simple, to switch to another EMS supplier — the customers will have to go through the entire process again [Design > Prototype > Testing & Validation > Production] which is time consuming. And time = money.

Business Opportunities & Growth Drivers

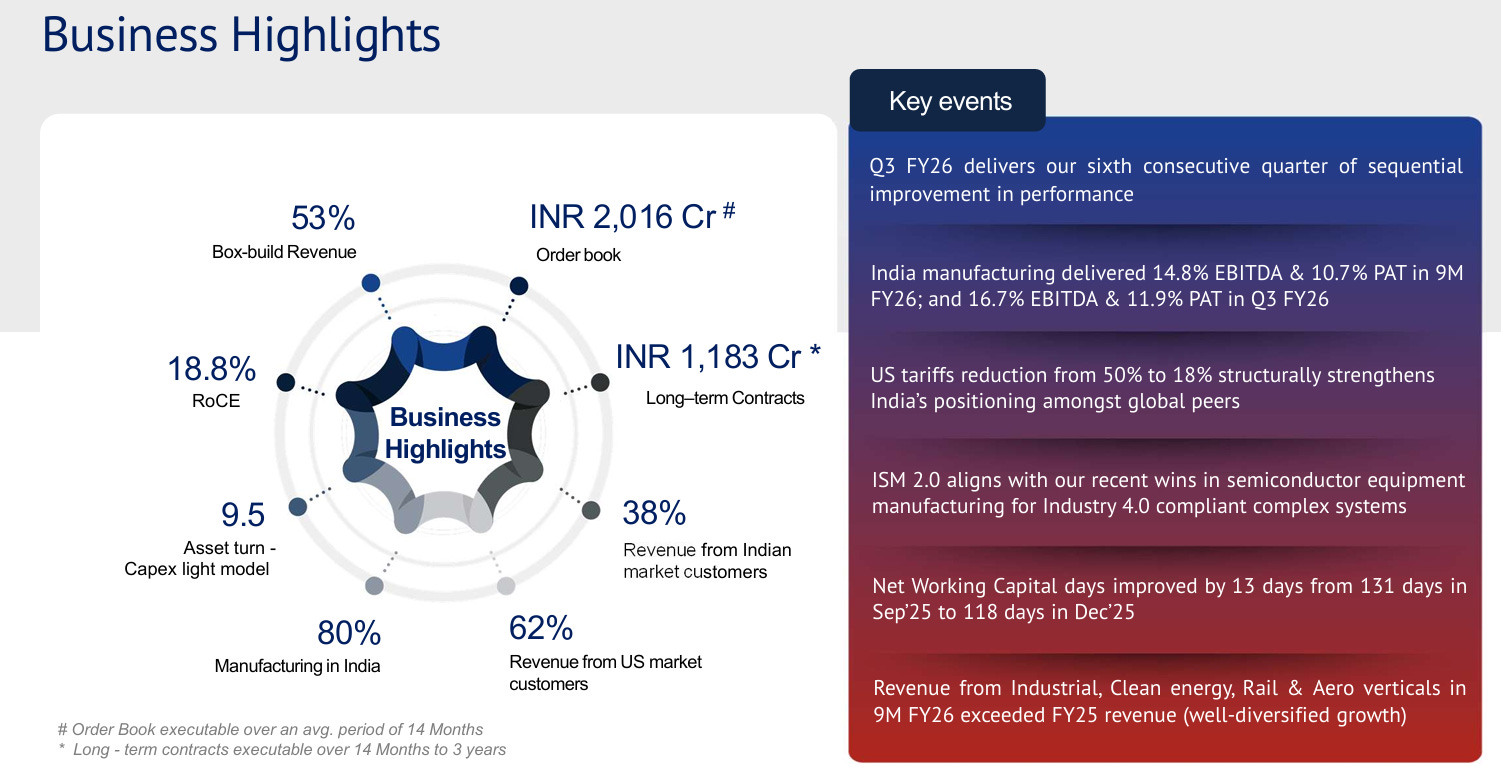

On 31st December 2025, Avalon had an order book of INR 3,200 Cr executable over a period of 3 years — which is 3x FY25 sales, offering good revenue visibility.

But, as an investor — you should be interested in the order book that is not quantified. Order book which is invisible to the markets. The potential revenue that could flow to Avalon, based on various projects that it is dabbling in. That’s where the alpha is.

Let’s look at some of the exciting projects that Avalon is working on.

Semiconductor opportunity — Avalon has onboarded a semiconductor equipment manufacturer as a customer and will provide box build solutions that will go inside semiconductor equipments. Avalon has completed the project readiness phase ahead of volume production and expects meaningful revenues from this segment from FY27. THIS IS A MUST WATCH GOING FORWARD!

Each of these machines cost $2-$3 million and Avalon will be making small parts which will go inside these machines. The management hasn’t given any number but expects it to be a BIG opportunity and is already in conversation with a second customer in this segment.

Other business opportunities:

Avalon completed its first tranche of prototypes to manufacture control units for satellite antennae systems. [Expecting volume orders in FY27 - number undisclosed]

Prototypes for industrial processing sector and power sector have commenced.

Onboarded new customers across industrial and defense segment for products like mission critical power inverter platforms, critical components for integrated battlefield command systems.

Ramping up the energy storage systems program and making steady progress in aerospace cabin assemblies.

Bidding pipeline:

The company is bidding for projects in advanced metal cockpit assemblies + landing gear components [Aerospace segment]

On the cusp of foraying into cable commodities [Aerospace segment]

The management has not placed any revenue number (#) on these opportunities, so it is anyone’s guess how much money Avalon will make from these projects or whether these projects will actually materialize — which is what makes it fun to track this company.

Green Shoots

Insulated from tariffs? — One of the things that impressed me reading the Q3 earnings transcript was the fact that Avalon was able to recover 99% of the impact of higher US tariffs from its customers — reflecting a strong and long-standing relationship it has built with its customers.

The way the company dealt with high tariffs (50%) was commendable. Avalon has 2 manufacturing facilities in the US, enabling it to deal with an uncertain tariff regime in the future as well.

With Trump in-charge, predicting the future is a fool’s game. All possibilities are on the table!

Now that the tariffs have reduced from 50% → 18%, Avalon finds itself in a favorable position to win more business.

Guidance — The management revised its FY26 revenue guidance upwards from 28% growth → 40% growth, a positive trend. No specific revenue guidance for FY27 was given. EBITDA will continue to remain in the range of 10-12%.

Number-gasm — Increase in ROCE from 11.3% → 18.8% YoY. Reduction in working capital days from 130 days → 118 days. Negligible debt to equity. Asset turnover improved to 9.5 times reflecting operational efficiency. US manufacturing facility remains loss making.

Conclusion

At a P/E of 70+ times, Avalon is not a cheap stock to own at these levels. Plus, promoters have been selling some part of their stake every quarter, signaling profit booking.

A high DII shareholding means that mutual funds will rate Avalon as a BUY, diverting retail SIPs into the stock, offering little space for the stock to correct from here, hence this is not a value buy.

What makes Avalon a lucrative company to own, is the future potential, which the market has already factored in to some extent, leaving little money on the table at current valuations. The semiconductor opportunity is a BIG one, which will materialize in FY27 and beyond. The company is dabbling in many other projects.

The question is — can Avalon surprise the market with its future projects, the value of which is not known at this moment in time but will be revealed in the foreseeable future? Can it become an EMS behemoth like Dixon in the next 5-7 years?

That is where the bet needs to be placed.

If you liked this article, share it in your investing network. Comment, like, show some love! I spend a lot of time in research & it would mean the world to me if you could recommend this blog to your friends.

[Note: The author is not a SEBI registered investment advisor, and the contents of this article do NOT constitute investment advice. Always do your own research before you invest in a company]

These EMS stocks always trade at high PE multiples. Returns can only come through earnings growth. Rerating potential is almost zero in such companies. You mentioned switching cost is there, i think this is the reason why market gives high multiple to such companies.