In the previous article ‘Betting on Space [Part 1]’ — I explored the potential of the Indian space industry and analyzed two stocks [L&T and HAL] that would give investors some exposure to the underlying growth of the space industry.

However, these two stocks have a pretty sizable market capitalization already — which means that investors cannot expect multi-bagger returns (15X or 50X or 100X returns) from these stocks. I spoke about L&T which has a market capitalization of > INR 4 TRILLION. If you invest in L&T today, for your investment to double, L&T’s market capitalization needs to be INR 8 TRILLION — which means that L&T will have to figure a way out to generate additional 4 trillion in profits. After a point, it becomes VERY difficult to scale a business.

Opportunity lies, in midcaps + small caps + microcaps. The risk is exponentially higher too. You wouldn’t see the stock price of HAL drop by 20% in a single day. But, with small caps that can happen frequently. Wealth can be wiped out and wealth can be created.

And it is this intricate game, that we must play.

With that, let’s look at some other opportunities that could take your portfolio to the Moon.

#3 Centum Electronics

Since #1 & #2 were covered in the previous article, I’m starting with #3.

Centum operates in the field of electronics manufacturing and technology solutions. It focuses on subsystems, micro-electronics and system integration services and has a significant presence in India’s space sector.

The company delivered > 200 mission critical modules and systems for the Chandrayaan-3 mission.

The company has presence in other sectors like Defense & Aerospace, Transportation, Automotive, Energy & Infra, Medical and Communications. It caters to customers across industries which includes DRDO, ISRO, Defense PSUs and various global OEMs.

Here’s how Centum Electronics makes money:

Electronic Manufacturing Services [EMS]: Centum offers manufacturing solutions like Printed Circuit Board Assembly (PCBA), complex finished products and complete system integration. If you’re someone with a design and you don’t want to invest in setting up an electronics manufacturing facility — you go to Centum.

Engineering R&D: If you want to manufacture an electronics product, you first need a design. The design will decide how multiple components will be assembled, the features, functionality of the product etc. If you’re struggling with the design — Centum can help you with that as well.

Conceptualizing & designing electronic hardware, embedded software, power electronics, radio frequency products — Centum has it’s fingers dipped in a lot of use cases.

Built to Specification [BTS] : Centum takes it one step further by offering you services of taking projects from conception to mass production quickly. Since they’re already into EMS and Engineering R&D — this plays in well for Centum to create their own ecosystem.

Primarily caters to the domestic defense & space sector (PSUs, Ordinance factories, DRDO etc.) and railway projects globally.

Margin profile of business segments, explained on an investor call (hypothetical conversation between ISRO <> Centum)

ISRO scientist: Guys, we need a sub-system that can monitor the propulsion module. It should have X functionalities. We can send you the design where this system will be housed, but the rest — is upto you.

Centum application engineer: Sure, no problem. We’ll plan the engineering sprints to complete and deliver this sub-system with the required functionalities. We’ll send you the commercials in sometime. P.S. Jai Hind!

Pros:

There are a lot of industry tailwinds when it comes to electronics manufacturing with estimates of EMS becoming a $100B industry in the next 4-5 years. Centum caters to hi-growth sectors like defense, aerospace, space, energy, mobility etc. and could be a key beneficiary from the growth in these sectors.

Centum has 25+ years of domain expertise in electronics design and manufacturing. The industry has a high entry barrier and requires precision engineering. This should mean sticky customers. More pricing power. Better margins.

They have experts in the fields of radio frequency, microwave, power electronics, digital design, electronic warfare.

Able to do micro-electronics manufacturing, which is a capability not many other companies in India have at the moment.

The management expects EV + Cleantech to be major growth drivers and China + 1 strategy working in favor of the company.

Healthy revenue mix with customers from various industries which safeguards the company from a downcycle in a specific industry. 75% revenue from exports to customers in UK/US.

The company has an order book of INR 1,542 crore [at 30th June 2023] which is around 1.6x FY23 revenue and gives visibility into future revenues.

Understanding Order book execution

Cons:

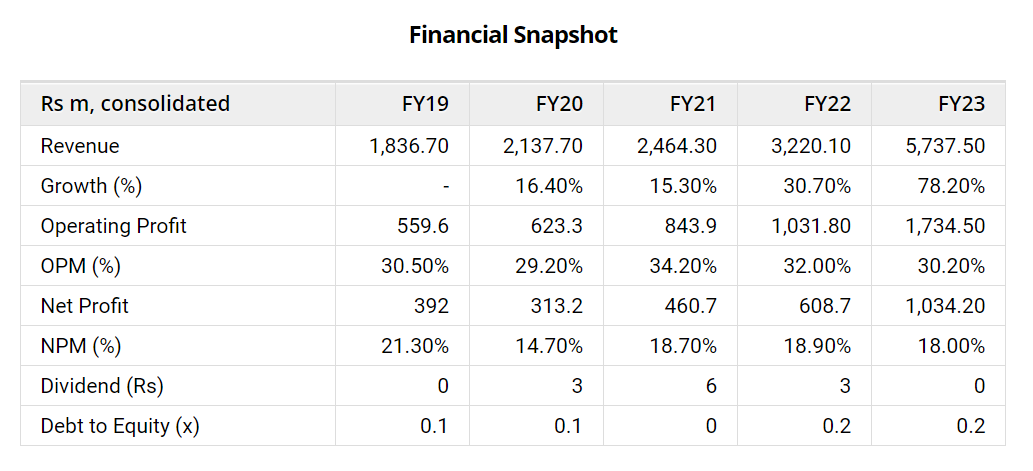

When I read 25+ years of domain expertise, my first thought is that the operating margins of the company should have increased over time. The reverse has happened with margins hovering around 8-9% for the past 3 years. Centum is unable to exercise pricing power with customers even though 75% of revenue is from exports to UK/US — geographies that enjoy high margins? Something looks off.

The management expects that the EBITDA margins for FY24 would stabilize around 10% and have guided for margins in the mid-teens regions (13-15%) over the long term. Would be interesting to see how this plays out.

One of the foreign subsidiaries of the company is making losses due to cost overruns and fixed price contracts [which has impacted the consolidated PAT]. Despite losses, the company has increased it’s shareholding in the subsidiary and expects to turn things around in the next few quarters.

Numbers needing improvement.

Players in the EMS industry have to continuously invest in capacity expansion (for higher growth + higher revenue) and a key metric to look for is ‘Return on Capital Employed’ — which tells you how prudent a company is in deploying its capital. Centum’s RoCE is around 6-8% for the past 3 years. Again, not very impressive.

75% revenue from exports exposes the company to downturn in the western economies + forex fluctuations. We’re currently witnessing a looming recession in Europe/US, and that could affect demand from outside India.

Borrowings have increased from INR 263 crore in FY23 to INR 298 crore as at 30 September 2023 — mainly on account of Capex and working capital requirement.

5Y sales CAGR of 3% signifies stagnant sales growth. Either volumes are stagnant. Or they’re unable to increase prices for their services. Or they’re unable to win new customers. Or they’re unable to complete projects quickly.

Comparison with Peers [Source: Screener.in]

At a P/E of 170, the stock looks extremely expensive especially with stagnant sales growth, low ROCE and low operating margins. The stock has already delivered 100% YTD returns and I’d suggest to keep this in your watchlist and track the quarterly results before taking any decision.

#4 MTAR Technologies

MTAR is in the business of manufacturing machine equipments, assemblies / sub-assemblies and spare parts for clean energy, space, aerospace, defense and other engineering industries.

It has 7 manufacturing units with plants strategically located near major defense organizations.

MTAR made significant contribution to the Chandrayaan-3 mission by manufacturing core parts of the rocket engine and core pumps of cryogenic engines which are required for take-off. It offers hi-tech products to ISRO like:

Liquid propulsion rocket engines

Cryogenic engine sub-systems

Electro pneumatic modules

Critical structures like grid fin (to be used in Gaganyaan missions)

I’m not an aerospace engineer, but the list above sure looks pretty impressive and would help MTAR build a strong relationship with ISRO. MTAR has supplied products which have been used for the Aditya L1 mission.

MTAR signed an MoU with IN-SPACe for design and development of a low earth orbit (LEO) all liquid small satellite launch vehicle powered by semi cryogenic tech with a payload capacity of 500KG. Whew, that’s dense.

So, a lot of exciting developments happening at MTAR when it comes to Space — however the company caters to other segments as well (see chart below)

Clean Energy: caters to manufacturing of power units, hot boxes, hydrogen boxes and electrolysers. Most of the sales in this segment is to a single customer — Bloom Energy.

Nuclear Energy: pertains to manufacturing of complex components and assemblies for nuclear reactors. Customers include BARC, NPCIL, Department of Atomic Energy.

Defense and Aerospace: supplying hi-precision indigenous components, subsystems for strategic missile programs. Boasts customers like Rafael, Tata Group, Collins Aerospace etc.

Pros:

Operates in high growth segments. Revenue grew by 78% in FY23 and the company expects revenue growth of 45-50% in FY24 as well. Order book stands at INR 1,078 crore [as at 30 June 2023] and the company expects an outstanding order book of INR 1,500 crore at the end of FY24.

Breakdown of Order book as at 30 September 2023 Execution of the order book — for clean energy it is much quicker (within 12 months) whereas for space / defence projects the execution time is anywhere between 1.5 - 2 years.

Domestic sales was around INR 50 crore in H1FY24, the management expects 3X growth in domestic sales in H2FY24 (INR 130-150 crore) which should have a positive impact on EBITDA

Operating profit margins are stable at 30%. Net profit margins look healthy at 18%. ROCE at 22%. I would like to see if MTAR can maintain / expand margins further in the next few quarters.

On 30 August 2023, MTAR received a defense industrial license which will enable it to produce various mechanical and electronical sub-systems for the defense sector. This should increase revenues from the defense segment going forward, which is currently a very small portion in the total revenue mix.

The management expects strong order inflow in the defence segment in the next 1.5 - 2 years. The company has received orders from NPCIL, which should get converted into revenues in FY26.

The company is in the pre-qualification stage of the SSLV technology — this could be a growth driver for MTAR in the future.

The company is well positioned to capitalize on import substitution opportunities for ball screws, roller screws, actuators etc.

Once MTAR receives the required clearance from various agencies, it should be able to supply electromagnetic actuators. Estimates suggest requirement of around 300-400 screws over the next few years. No additional CAPEX would be required to undertake this development.

Extract of investor con-call for Q2FY24.

MTAR is investing in capacity expansion by establishing units in Europe/US for energy storage systems. Once these facilities are up and running and the capex cycle is complete, it could significantly boost revenues.

Cons:

MTAR derives 69% of it’s revenues from a single sector — clean energy. Out of this, Bloom Energy contributes close to 50% of total revenues. Any adverse impact / slowdown in the business of Bloom Energy could directly impact MTAR.

This is evident from the Q2FY24 results. The company had pulled back it’s FY24 revenue guidance from INR 860 crore to INR 700 crore due to deferral of shipments to Bloom Energy because of a shift in model (from Yuma to Santa Cruz Block Block 2 — which resulting in energy efficiency for Bloom)

Also, what is important to note — is that MTAR is NOT the sole supplier of Bloom. It currently caters to around 70% of the demand for hot boxes for Bloom, and the rest is fulfilled by a company based out of Taiwan [name of the competitor not specified in the investor concall.]

The management has revealed that they have added new customers in the Clean Energy space but have not specified the name of such customers. It would be extremely important to see if they can de-leverage themselves from Bloom Energy in the long term.

The company has also pulled back it’s EBITDA guidance from 28% to 26% (+/- 1%) for FY24.

Derives 80% revenue from exports [since Bloom Energy operates in the US] which exposes MTAR to forex fluctuations. Slowdown in US/Europe — which is currently underway — could impact the topline of the company.

Revenue breakup — exports vs domestic sale. Working capital days stand at 230 days [at 31 March 2023]. Inventory and Trade receivables have significantly shot up in FY23 which could strain the cash flows of the company. Cash balance [at 31 March 2023] was only INR 31 crore.

For Q2FY24, there has been a sharp reduction in payable days, impacting the cash flow from operating activities.

Borrowings have increased by approx. INR 108 CRORE — the reason of which was not explained either in the investor PPT / concall.

Working capital movement QoQ.

Promoter stake in the company has been decreasing. MTAR’s stock has run up significantly in the past few months, and a few promotors have used this opportunity to cash out. Not a good sign, since that shows that the promoters think that the stock might be overvalued.

All in all, I think MTAR has a lot of positives. It’s making some good inroads in the space and defense business. Revenue growth has been spectacular in FY23, which is expected to continue. Order book looks strong and is estimated to grow significantly — which if it happens — would reflect positively on the strength of the business.

With a market capitalization of INR 6,600 crore — the stock is trading at a P/E of 64 times, which is a little expensive for my liking. I would like to see customer concentration going down and more business picking up in the defense and space segments to reduce the reliance on the clean energy space.

That said, MTAR definitely deserves a place on your watchlist. In case the stock falls by 15-20% from the current levels, it will look very attractive as an entry point for a long term investment.

There are lots of other space stock to cover — like Linde India, Paras Defense, Avantel, Astra Microwave, Bharat Forge etc. Stay tuned to see which one makes the cut!

If you liked this article, share it in your investing network. Comment, like, show some love! I spend a lot of time in research & it would mean the world to me if you could recommend this blog to your friends as well OR you could contribute by donating a small token to fund my research!

[Note: The author is not a SEBI registered investment advisor and the contents of this article do NOT constitute investment advice. Always do your own research before you invest in a company]