When I think of Raymond — an image flashes in front of me. An alpha male, wearing a fashionable blue suit, walking with intent, flexing his expensive wristwatch, ready to conquer the world.

The brand exudes style, quality & sophistication. It’s a symbol of luxury. Of premium clothing.

However, Raymond has two other business verticals as well — Engineering & Realty — and in a bid to unlock shareholder value, the management at Raymond decided to de-merge these verticals into 3 distinct listed companies as below:

Raymond Limited — which houses the engineering division.

Raymond Lifestyle — which houses the textiles business, the brand that everyone knows.

Raymond Realty — houses the real estate business, with a primary focus on the Mumbai real estate market. A very lucrative market.

Since the de-merger, the share prices of all 3 companies have heavily tanked. In the last one year — Raymond Limited is down 15%, Raymond Lifestyle is down 25% and Raymond Realty (RRL) is down >60%.

As an investor, when you see a 60% drop in a stock — you could assume several things. Maybe the business isn’t doing well. Projects must be stuck for regulatory approvals. Profitability must be low. Cash flows must be negative. Return ratios must be in low single digits. Management could be involved in fraudulent activity.

In short — you’d assume a management that isn’t equipped to be in the business of running a real estate company. Maybe Raymond should stick to selling premium clothing? [which isn’t doing that great either btw!]

However, if you go through the Q3 earnings transcript a very different picture emerges. The numbers look solid. You meet a management that is confident in their execution capabilities. Promoter buying in the wake of declining share prices. A decent ROCE and a solid order pipeline.

WHAAAT?! These are not signals you get when a stock drops by 60% in a single year!

I was definitely intrigued, and I couldn’t help myself but conduct a deeper dive into the business of Raymond Realty [RRL].

What makes it a value opportunity?

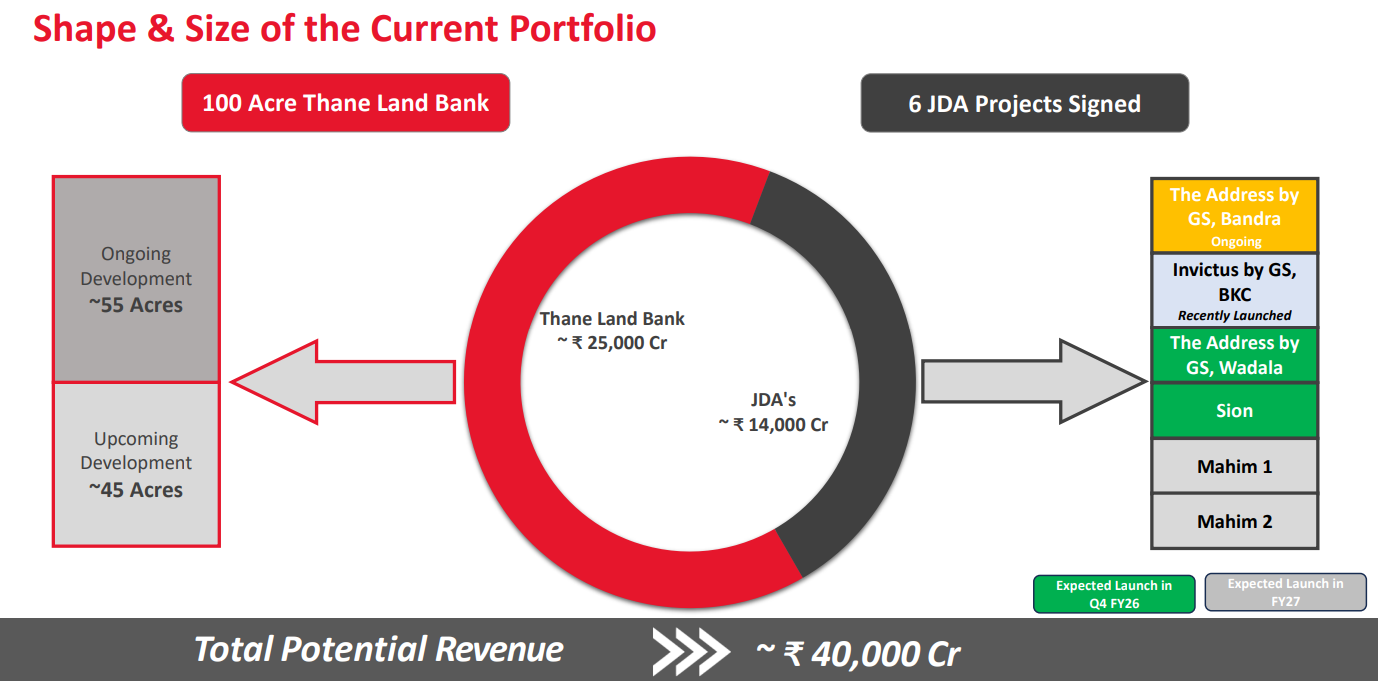

One of the biggest advantages working in the company’s favor — is the 100-acre land bank it owns in Thane. It’s their turf. They don’t have to worry about regulatory clearances. No additional costs need to be incurred to buy this land + Thane is a fast-growing area with a lot of infrastructure being built [read: new metro lines]

The management estimates a [cumulative] revenue potential of INR 25,000 Cr from this 100-acre land bank. Out of this 100-acre land, 55 acres is currently under development with a GDV [revenue potential] of INR 13,200 Cr.

To grow beyond Thane, Raymond Realty is partnering with landowners in other parts of Mumbai — Bandra, Wadala, Sion, Mahim etc. — under a Joint Development Agreement (JDA).

Most of these JDA projects are redevelopment projects — where an old building is demolished and a new building is built in its place.

Under a JDA, the landowner provides land to a developer (like Raymond Realty). The developer doesn’t have to pay to buy land or bear any of the costs associated with buying a land.

The developer takes care of the construction, RERA approvals, sales etc. Profits are split between the landowner and the developer. This is a good strategy to grow without acquisition of land parcels especially in a city like Mumbai where land is scarce.

A JDA project has faster execution; hence developers are able to rotate cash faster leading to higher ROCE %. However, margins are lower compared to a greenfield project.

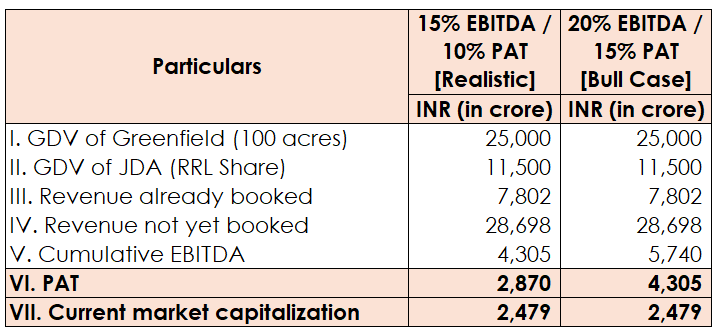

If you take a look at the table above, you can see that cumulative PAT in the future > current market capitalization. And these are conservative estimates. As per the latest earnings call, the management expects EBITDA to hover in the range of 20%.

Now, the market already knows this. It is way smarter than people like you and me. The market doesn’t care about the GDV or the potential of JDA projects. It strongly feels the management will not be able to execute on its promises. The brand is tarnished?

I don’t have insider knowledge to understand why the stock is beaten down to such levels, but there are a few things which could have contributed to the decline:

Compression in margins post de-merger — before it’s demerger, the realty business was posting EBITDA margins of 25%+ and post demerger margins have compressed to 13%.

Management explained that before the demerger, the realty business was a business unit, and a lot of common costs were not allocated to the realty business — hence elevating the margin % before the demerger.

Another thing dampening margins is the upfront investments / expenses required in the current projects — with two JDA projects already launched and 4 more projects in the pipeline. As the projects mature, EBITDA should stabilize.

All Raymond entities are down post demerger, and the brand name is under a lot of stress — weighing down on the realty business as well, however what’s going on with the Engineering / Lifestyle businesses has no direct implication on Raymond Realty.

Project launches in pipeline

4 launches are planned in Q4FY26 — out of which 2 projects are JDA projects outside the Thane market [Wadala + Sion].

The Address by GS [Wadala] — located in Wadala, this project was launched in January 2026 and has a GDV of INR 5,000 Cr. RERA filings indicate a 62:38 split in favor of RRL, so out of the total GDV — around INR 3,100 Cr should be recognized by RRL.

The Address by GS [Sion] — located in Sion, this project was launched in February 2026 — as committed by the management.

Launching two other greenfield projects in Thane — one is a project targeting the 2BHK community and the other is a high street retail project with high margins, which the management believes should help the company achieve the revenue numbers & margin profile forecasted.

Guidance

Management expects to grow revenue + pre-sales by 20% YoY. It is targeting a FY26 pre-sale of INR 2,800 Cr, out of which INR 1,500 Cr is booked till Dec’25.

The management was VERY confident on achieving a pre-sale of INR 1,300 Cr in Q4 — and were visibly annoyed when analysts questioned them on this number. If they achieve this number in Q4, that would be a validation of management walking the talk. Accurate forecasts are a rarity.

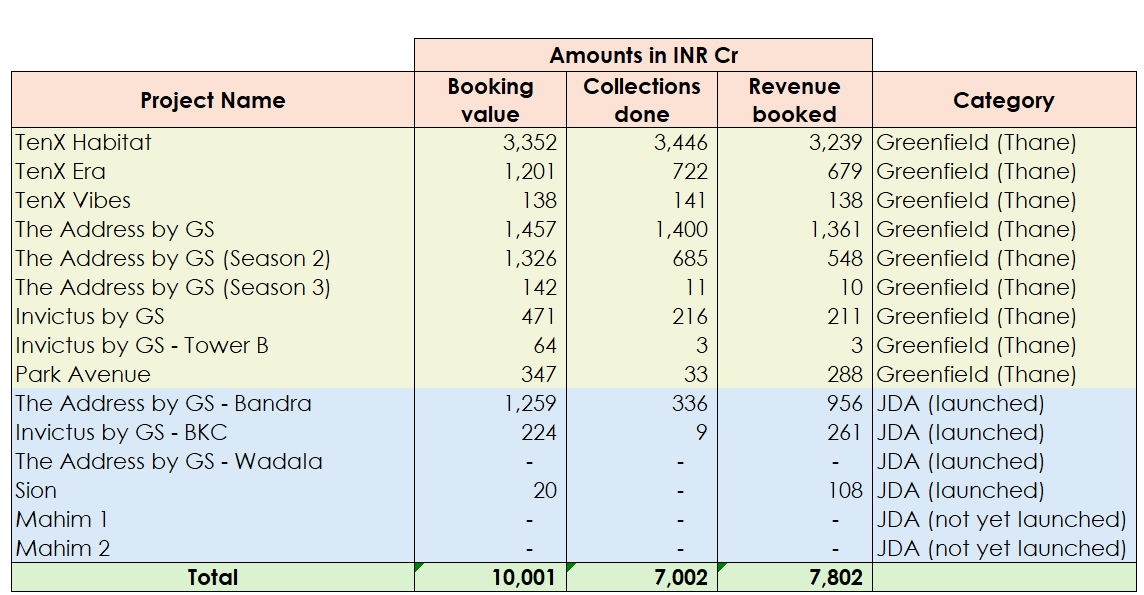

Post launch of 4 projects in Q4, the company would have 13 projects in total.

Expecting EBITDA to settle in the range of 15-16% by the end of FY26 and to further expand to 20% by FY27.

However, one thing to note here — is that going forward to unlock growth, Raymond is looking towards JDA projects [which are primarily redevelopment projects]. Currently 22% of pre-sale came from JDA projects, which should inch up to 50% of pre-sale by FY28.

JDA / re-development projects have lower margins compared to greenfield projects and it would be interesting to see how the company manages to maintain a margin profile of 20%+ in the foreseeable future with the mix of JDAs increasing.

My take?

I’ve read only a couple of earnings call transcripts — but one thing is clear, the MD & CEO of Raymond Realty — Mr. Harmohan Saini — has character. He is confident about his commitments and forecasts. He’s been in the real estate game for over 30 years, and he isn’t shy to lead from the front.

The stock is down 60% — I don’t see any obvious red flags in the business. They have a massive land bank in Thane, they’re getting into JDAs — yes, its not the sexiest business to be in [like semiconductors / AI / biomedicine] — but at the current valuations, I see limited downside. And I see a LOT of upside.

The Iran-Israel-US war has dampened investor sentiment in general and portfolios are bleeding red. But this is an opportunity to scoop up good businesses at a discount — and I believe RRL deserves a closer watch.

If you liked this article, share it in your investing network. Comment, like, show some love! I spend a lot of time in research & it would mean the world to me if you could recommend this blog to your friends.

[Note: The author is not a SEBI registered investment advisor and the contents of this article do NOT constitute investment advice. Always do your own research before you invest in a company]