Can Atlanta Electricals become a large cap transformer player?

and paying attention to the business of transformers

India’s power requirement is steadily inching up — given the growth of new technologies like AI, EVs, battery energy storage systems along with a general push for ‘Make in India’.

More manufacturing = More factories = More power requirement.

I read an interesting article by ‘the Megatrend Investor’ which speaks about how this is going to benefit companies manufacturing transformers.

It is not enough to generate power, but you also need the ability to transmit that power to where it is required. Transformers play a very important role in transmission of electricity — which is why you’re seeing most of the transformer companies in India increasing manufacturing capacity.

The primary purpose of a transformer is to change the voltage of electric current. Without a transformer, electricity transmission breaks.

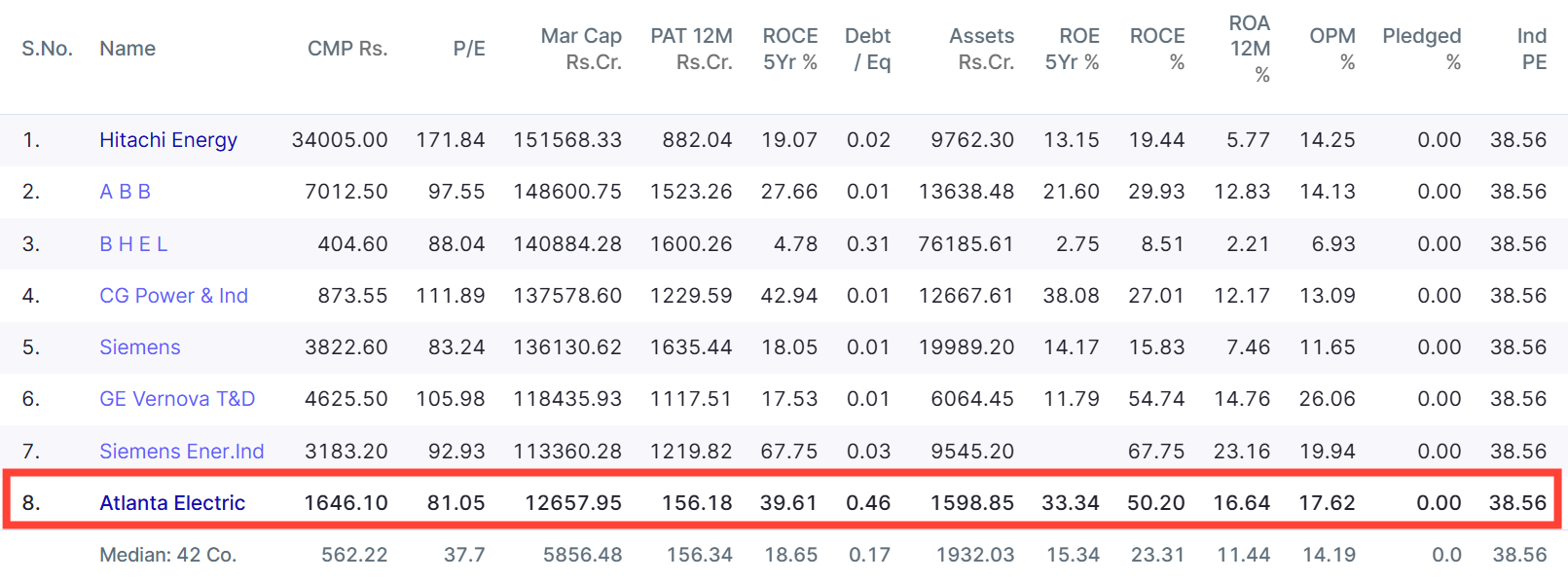

Various companies in India manufacture transformers like BHEL, ABB India, Siemens, Hitachi Energy — which are massive companies. A few mid-cap players like Atlanta Electricals & TARIL also operate in this segment.

I generally avoid spending time analyzing companies in the large cap category — because the probability of them generating multi-bagger returns is quite low.

In this blog, we will learn about the growth potential of Atlanta Electricals and strive to understand whether the management of Atlanta has what it takes to scale and become a large cap transformer company.

The Business Model

Atlanta Electricals was incorporated in 1983 with its HQ in Anand, Gujarat. It manufactures different types of transformers like power transformers, invertor duty transformers, auto transformers ranging from 5MVA/11kV to 500MVA/765 kV.

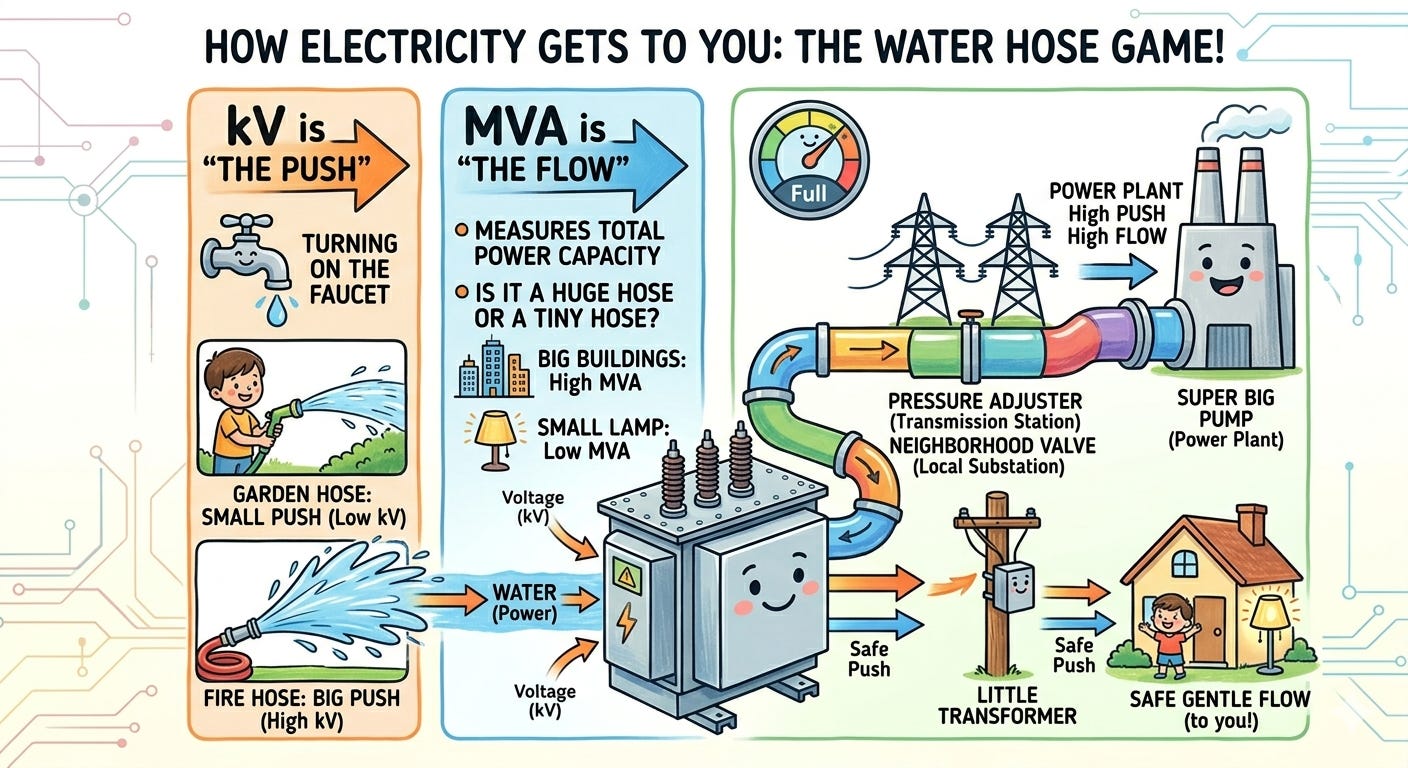

Electricity terms you should understand:

(1) kV = kilovolt. It denotes the voltage that a transformer can handle.

(2) MVA = megavolt-ampere. This is the volume of electricity a transformer can handle at any given point in time.

The company has 5 manufacturing facilities with a total capacity of 63,000 MVA and caters to a diverse customer base with notable names like Adani Green, Tata Power, GETCO and other utilities.

In the last 18 months, the company has invested heavily to increase capacity from 16,000 MVA → 63,000 MVA — in line with the industry trend.

Order Book

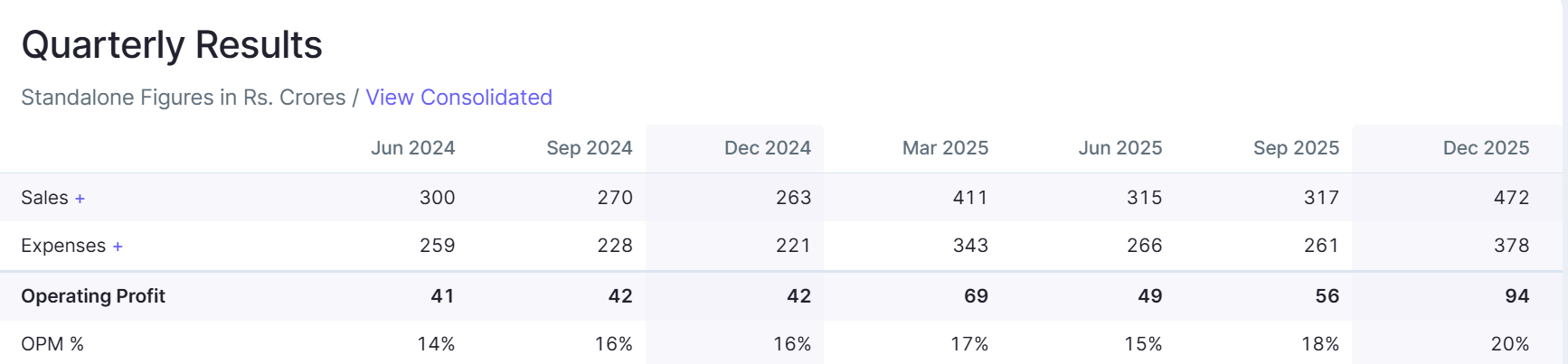

On 31st December 2025, the company’s order book stood at INR 2,451 Cr [2x of FY25 revenues] giving strong revenue visibility. Management expects this order book to be executed in the next 18 months.

The company has a bidding pipeline of INR 10,000 Cr with a hit ratio of 10-15%.

The quarterly order inflow of the company is around INR 700 Cr.

Q3 order book wins:

Secured orders worth INR 298 Cr from GETCO for 25 high-capacity transformers.

Won orders worth INR 134 Cr from Adani Green Energy for supply of inverter duty transformers.

Secured marquee EHV (Extra High Voltage) orders from BNC Power for the Pugal project.

Secured orders worth INR 116 Cr for solar pooling substations across Bikaner, Bijapur and Pugal projects.

Capacity Expansion

Most of the players in this space have increased their manufacturing capacity, and Atlanta was no exception increasing its manufacturing capacity from 16,000 MVA → 63,000 MVA.

The company’s facility in Vadod (Unit 4) commenced production in July 2025 — which is designed for transformers up to 500 MVAs. This plant enables the company to undertake higher ticket size orders.

The Vadod facility was running at 30% capacity — generating INR 160 Cr in revenues [approx. 30% of Q3 revenue]. As capacity utilization increases, this should result in expansion of revenues. This is a metric to be tracked.

Operating margins increased in Q3 due to higher output from the Vadod facility — where 220kV class of transformers are being manufactured which command higher margins.

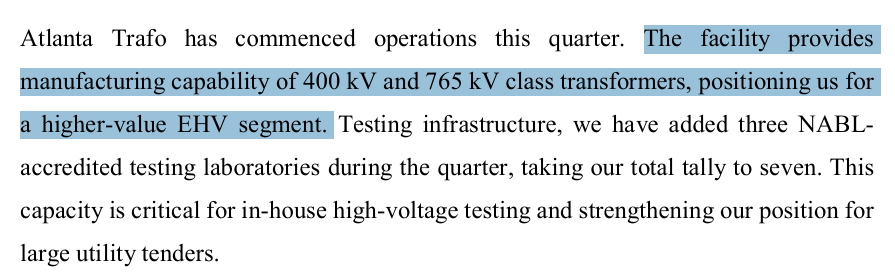

Atlanta Electricals acquired Atlanta Trafo Private Limited (ATPL), with acquisition of 90% of shares of BTW and subsequently ATPL became a 100% subsidiary of the company.

The facility at ATPL (Unit 5) has a capacity of 15,000 MVA with provisions to increase it to 45,000 MVA — however the management has not commenced such expansion yet.

Unit 5 provides capabilities to manufacture 400 kV and 765 kV class of transformers — which are high value, command higher margins and are categorized as Extra High Voltage (EHV). These transformers are difficult to make and places the company in a niche category of players with the ability to do so.

Guidance & Future Outlook

The management has maintained a growth rate of 40% — and look on target to achieve it for FY26. The bigger question is, can it maintain such a high rate of growth in the years to come?

Revenue by class of transformers — 220kV (45%), 132kV (19%), 66kV (32%) and others (4%)

The company is working on prototypes for 400kV class of transformers, and once it is able to execute the first few orders of 400kV transformers — the company enters a whole new ballgame. 400kV transformers command better margins compared to 220kV transformers.

The management expects order book to further rise, as 400kV orders last for about 2 years.

Atlanta recently received approval from PGCIL to manufacture transformers up to 400kV at its Vadod facility. This strengthens the company’s ability to apply for EHV tenders — which is a high value, high margin business.

It remains to be seen how quickly Atlanta can scale the EHV segment — and how margins and revenue expand as a result of this transition. Can Atlanta compete with the industry giants?

If it can, the stock price could further shoot up from here.

Conclusion

At a P/E of 80+, the stock doesn’t offer a cheap entry point. It is definitely expensive at current levels. The question is, can profitability expand? Can order book + revenues keep growing at 40%?

The 5Y ROCE is around 40%, which means that the management runs a tight ship. This is a number that tells you a lot.

Debt levels have inched up due to high capex activity in the last few quarters — management expects to repay some of the long-term debt in Q4.

At a market capitalization of 12,600+ Cr, there could be more room for growth. Other transformer companies [the GIANTS] do not give you that cushion. The probability of generating multi-bagger returns from BHEL, ABB, Hitachi is very low.

Atlanta Electricals listed on the markets on 29 September 2025 and has delivered 2X returns so far.

The company is at an inflection point, where it has built the capacity to get into the EHV segment. Prototypes are ongoing, and the future growth hinges on how much of a mark the company makes in this high value segment.

The management looks capable, and I like the fact that promoters hold more than 87% of shareholding in the company. The promoters have not booked any profits despite the stock zooming up. This is a signal of strong promoter conviction in the future of the company.

The demand for power is on the rise, as India adds more data centers for AI, builds EV charging infrastructure, makes progress in the development of green hydrogen and in general, promotes more businesses to ‘Make in India’.

All of this translates into more demand for transformers and whether Atlanta can make the most of this multi-decadal opportunity remains to be seen.

If you liked this article, share it in your investing network. Comment, like, show some love! I spend a lot of time in research & it would mean the world to me if you could recommend this blog to your friends.

[Note: The author is not a SEBI registered investment advisor, and the contents of this article do NOT constitute investment advice. Always do your own research before you invest in a company]

Any comments on transrail lighting ltd