Modern warfare, has undergone a gigantic shift. The outcome of a war isn’t decided by which country has more tanks, fighter jets, or a bigger army — but which country has better missile systems, sensors and embedded electronics.

It’s a war between systems, computing power and cutting-edge micro-processors.

Unfortunate as it is, we’re very far away from global peace. War is brewing in various parts of the world and defense budgets are increasing.

Closer to home, we’ve seen the recent Indo-Pak conflict, where India’s air defense systems were thoroughly tested and has led to the Government pushing for greater domestic production of defense equipment.

India’s defense budget for 2025/26 is a staggering INR 6.81 LAKH CRORE, which could increase by further 50,000 Cr as a result of the recent Indo-Pak conflict. Stock prices of defense companies have exploded (pun intended) and as an investor, this is a sector you cannot ignore.

I’ve been tracking a small-cap company for quite some time [and I missed the bus!], where the management is making aggressive moves with the aim of becoming a fully integrated Tier-1 defense OEM.

Enter Apollo Micro Systems.

The company has delivered multi-bagger returns in the past 5 years, with the stock price up 70% in the last one month. Although the stock looks expensive at current levels (P/E of >100) — the management believes that there is a lot of room to grow from here.

Can the company keep multi-plying shareholder wealth in the future? Can it compete with bigger incumbents like BEL, BDL? Only time will tell. What we can do, is learn about how AMSL makes money and it’s growth drivers in the future.

The Business Model

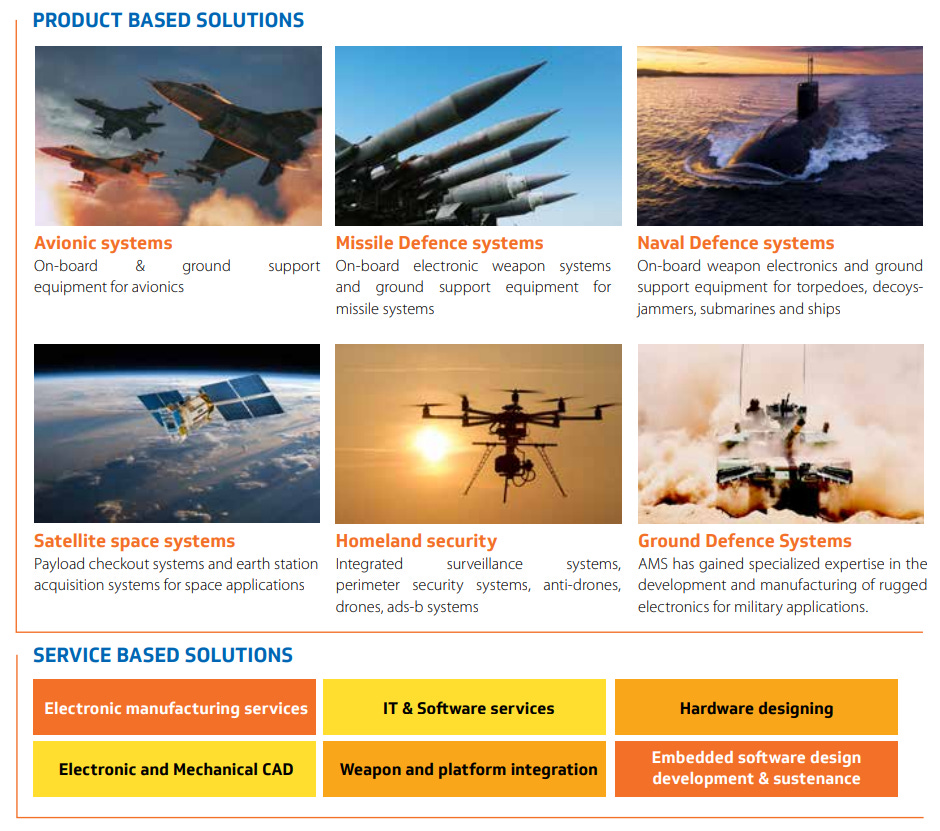

Incorporated in 1985 in Hyderabad, the company is in the business of design and development of advanced weapon systems catering to strategic domains like missile systems, satellite and space systems, naval systems, avionics and homeland security.

In short, it makes the ‘intelligence’ inside major defense equipments.

A brief history

It started as an electronic CAD design company in 1985. Entered the defense segment with processor boards in 1990. Launched telemetry products for ISRO in 2005. Configured automated launcher controller for AGNI missiles in 2010. Entered RF & Microwave designs via acquisition of established RF company in 2021.

Over time, the company has moved up the value chain — designing its own systems, partnering with state-run giants and expanding across land, sea, air and even underwater defense systems.

The Model

Development of a weapons system requires years of R&D, testing, inspection before it is approved for large scale production. Scrutiny & inspection is involved in every stage of production, starting from raw material procurement to delivery of the systems.

Therefore, there is a high barrier to entry in this industry. Customers are sticky, because it is not easy to switch weapons systems. Significant capex is required in setting up manufacturing, R&D and testing facilities. Major raw materials are semiconductors and high-speed microprocessors, which are the brains of the weapons systems.

The company has participated in 150+ indigenous defense programs over the years and has >700 technologies on the table.

However, longer development cycles means money stuck in inventory (like raw materials), putting a strain on working capital & return on capital. Defense contracts can be lumpy and unpredictable.

The Tailwinds

Apollo Micro Systems is part of the group of suppliers which are the backbone of modern defense in India. The company’s management is expecting revenue growth of 45-50% YoY over the next 2 years — indicating significant tailwinds in the future.

Order book — As of May 2025, the company’s order book was INR 615 Cr. Management is expecting to triple this by the end of FY26 to INR 1,800 Cr. This is a metric that investors should actively track — giving confidence about management’s ability to achieve their targeted revenue growth of 50% every year for the next 2 years.

the company bagged a ₹113 crore export order for avionic systems (the electronics used in aircrafts).

Preferential issue — the company plans to raise INR 816 Cr via preferential issue of shares which will be utilized for working capital purposes, R&D expenditure, investment in subsidiaries and development of new innovative technologies.

Manufacturing ramp up — Apollo has one manufacturing unit [Unit I] located in Hyderabad over 55,000 sq ft and it is aggressively ramping up capacity.

Manufacturing units @ AMSL [Source: Investor PPT] Partial operations have started in the second manufacturing unit [Unit II] and full fledged manufacturing is set to commence from Q2FY26.

The company is investing in building a new weapons integration facility [Unit III] which will involve a CAPEX of INR 250 Cr and will be fully operational by the end of Q4FY26.

This gives you a hint that the management expects exponential growth in defense contracts in the future and wants to be ready to cater to that demand by building manufacturing capabilities upfront.

Sticky customer relationships — The company has a track record of ZERO customer attrition, partly due to the nature of the business which involves long development timelines and difficulty in replacing defense vendors.

Marque clientele of AMSL [Source: Investor PPT] High entry barriers coupled with the long term nature of defense contracts [extending over several years] provides revenue visibility over the medium term.

Robust R&D Team — the company invests close to 6-8% of revenue on R&D, with 165+ people working in the R&D team. FY25 resulted in successful development of aerial bombs, underwater acoustic sensors, critical actuation systems, secured data links and many other products.

Partnerships — the company entered into various partnerships which could open new doors and expand revenue streams:

Signed a partnership with Munitions India Limited to develop advanced weaponry.

Joined forces with Troop Comforts Limited to build anti-drone + anti aircraft systems.

Collaborating with private sector companies on drone landing modules, underwater mines and development of torpedo guidance systems.

Signed a MoU with Garden Research Shipbuilders for development of mini-torpedoes.

Acquisition — the company is in the process of acquisition of IDL Explosives Limited, which is engaged in the manufacture of full range of packaged & bulk explosives.

The strategy is simple — by acquiring an explosives company, Apollo moves into a league where they can manufacture the entire weapon (and not just its sub-systems)

Plus, there are not many companies in the explosives space. A few large players like Premier Solar and Munitions India and a bunch of very small players.

The company is going to increase its portfolio into warheads + rocket propellants + rocket motor designs through this acquisition. They will enter into a complete ammunition cycle where different calibers of mortar will be developed in-house and supplied to Indian defense forces which will have a huge export potential.

This acquisition, the management believes — would enable AMSL to transition into a fully integrated Tier-1 defense OEM.

Growth drivers — the company has dipped its toe into almost every indigenous development program in the country and is working on several promising technologies.

Sneak peek into some of the products made by AMSL. [Source: Investor PPT] Underwater mines — management expects this to be a BIG opportunity, with combat trials conducted and expecting order flows in FY26.

Submitted samples of moored mines to DRDO for evaluation, could translate into future orders.

Working on portable mines called Limpet mines for supply to the Indian Navy.

Heavy weight torpedoes — received financial approval from the Ministry of Defense for deployment of Varunastra, an anti-submarine torpedo developed by BDL (Bharat Dynamics Limited). Once BDL receives an order from the MOD, subsequent order to AMSL will be awarded to develop systems for Varunastra.

Expecting significant orders to flow in the advanced light weight torpedo (ALWT) category.

Received orders for limited production of electric heavy weight torpedoes (EHWT) from BDL. More orders expected in FY26. EHWT is being used in majority of the sub-marines.

PRACHAND Munitions — AMSL was shortlisted by DRDO for production and supply of PRACHAND munition hardware to Indian Armed Forces. PRACHAND is an anti-tank munition with full-width attack capability.

Air missiles — working on 4-5 subsystems which will be part of Project Kusha, a long range surface to air missile system. BEL is a key player for this project. Apollo has already supplied critical actuation systems and is developing launcher systems for this project which will be completed by Q2FY26.

QRSAM — is a short range surface to air missile system being developed by BDL, BEL and DRDO. The company is expecting large orders pertaining to QRSAM to come from BDL over the next 2Qs.

AKASH-NG — is a state of the art surface to air missile system designed to intercept high speed agile aerial threats. The management is expecting good orders in this category as well.

The company is working on other projects like AAD & ASTRA.

Points of concern

Underwater mines. Anti-submarine torpedoes. Anti-tank munitions. Surface to air missile systems. Apollo Micro Systems is working on exciting technologies, in an environment where defense spending is on the rise in India.

However, that doesn’t mean that everything is rosy. There are certain causes of concerns that an investor should be aware of.

Few projects in production — although the company is working on several technologies, the [BIG] money is made when a system transcends from development into production. The management acknowledged the fact that several dozens of programs are being done, but not many systems have gone into full-fledged production.

Stretched working capital — as we have seen, the company operates a business model where capital is blocked for a very long time. Long production cycles. R&D spanning several years. Delays in approvals. Projects can get stalled due to a bazillion reasons. All of this means, that a lot of money is required to keep things running.

Notice the high debtor & inventory days, which has a direct impact on ROCE. Customers pay only after systems are thoroughly tested, which results in high debtor days.

Not making any accusation here — but whenever I see high inventory & debtor days, my internal antennae goes up. If you study the history of financial manipulation, you’d see a direct relationship to these two metrics. However, in this case — most likely it is the nature of the business. Defense contracts require a large build up of inventory & it is NOT EASY to get money from government companies!

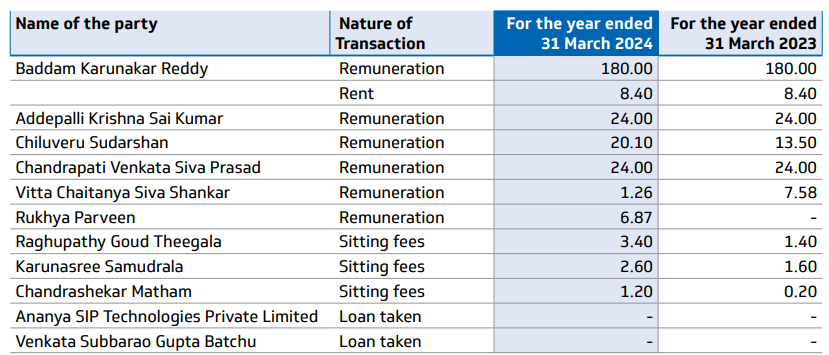

Employee expenses are abysmally low — for a company which boasts that it has not seen any turnover in the R&D department, employee expenses look very low.

RPT schedule of the company [Source: FY24 AR] the median remuneration of employees for FY24 was INR 4.7 lacs, which is quite low. In an innovative R&D defense tech company, you’d expect this # to be significantly higher. How are they going to attract top talent?

their CFO is getting paid only INR 20LPA — which is VERY low.

The company has a 3.6* rating on Glassdoor, which is decent. But for a company to scale exponentially, you would need highly motivated individuals which can bring forth innovative ideas. I’m not sure if Apollo Micro Systems, has too many bright minds working in their R&D labs at the moment.

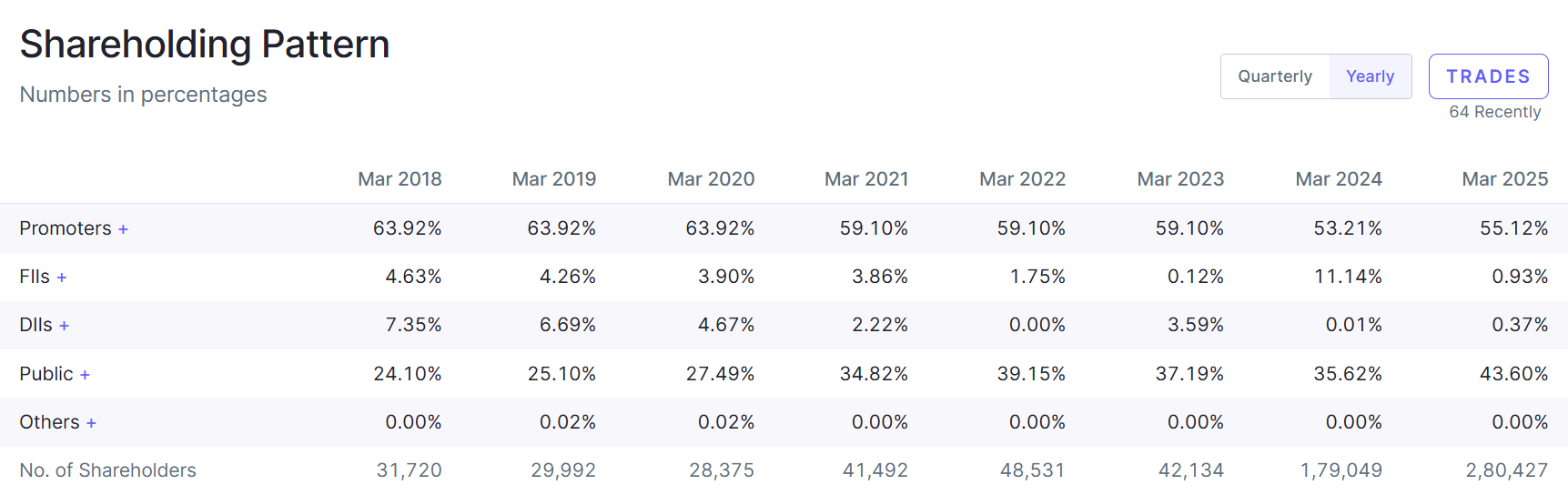

Promoter pledged shares — around 48% of promoter shareholding is pledged, which is an insanely high number. Management has explained that promoters have pledged shares to raise money to invest back into the business [I am not buying it] — which is a very risky strategy. A drop in stock prices of AMSL, could trigger margin calls from banks and could lead to a massive sell-off.

Low FII / DII holding — as retail investors, you have limited information to act on. FIIs / DIIs subscribe to their Bloomberg terminals extracting a LOT more information than we have access to. For small-caps in particular, a steady FII / DII holding gives comfort to retail investors. In the case of AMSL, FII / DII holding is quite low.

Shareholding pattern of AMSL [Source: screener.in]

Conclusion

I think the company has a lot of promise. Management has guided for a 50% revenue growth for the next 2 years on a standalone basis. A 100% revenue growth for FY26 if revenue of IDL Explosives is consolidated.

It is working on several exciting system developments. Acquisition of IDL Explosives, would steer it closer to becoming a Tier-1 integrated defense player. It is raising money for working capital and R&D. Building new manufacturing units. Growing its order book.

Some unanswered questions that I’d like answers to:

What is the manufacturing capacity of AMSL? What are the utilization levels? How much capacity is going to be added by Unit II and Unit III?

Can Apollo deliver projects worth > 1,000 Cr in a year since it takes such a long time to develop systems? How many projects are expected to go from development stage to mass production stage?

What is the breakup of product revenue? What are the best-selling products? Which product gives the highest margins?

What is the revenue breakup by customer? Is there a high concentration from 1-2 customers like BDL / BEL?

At a market capitalization of INR 6,000 CRORE, at a P/E of 106 — the stock does look expensive. I’d most likely take a small position in the company to track it’s performance and see if the revenue targets are being met in the next few quarters before building a larger position. The defense sector on a whole, is kicking things up a notch.

If you liked this article, share it in your investing network. Comment, like, show some love! I spend a lot of time in research & it would mean the world to me if you could recommend this blog to your friends.

[Note: The author is not a SEBI registered investment advisor and the contents of this article do NOT constitute investment advice. Always do your own research before you invest in a company]

Hi Siddharth....in this post I felt risk factors presently overweight the opportunity it offers that's why these need to sort out by company first. I am re-emphasizing these points like pledge shares with growing borrowing with stretch capital cycle. Kindly also include checklist in your analysis.

PE & PEG on higher side