A real estate player worth tracking ft. Raymond Realty

decoding the Q4 results + why I believe RRL could be a wealth creator in the years to come

I rely far more on gut instinct than researching huge amount of statistics ~ Richard Branson

Instincts play a crucial role in investing. You’re reading an earnings call transcript, and something just clicks in your mind.

Your [subconscious] mind is working in the background, asking questions like:

What is the tonality of the management? Are they confident about the business?

Can they execute on their promises? Are they trying to avoid any specific question?

How much can the business realistically grow? Can it compete? Can it expand margins? Can it build new products?

Is the management ethical? Can I trust them?

WILL THIS COMPANY MAKE ME A LOT OF MONEY?

You are not aware, but your subconscious mind is doing these calculations in the background. The more you learn, the more powerful your instincts get.

And it would do you a world of benefit to listen to your internal voice. It knows things you cannot explain.

Obviously, acting on your instincts doesn’t mean you can avoid the legwork. You must do a thorough analysis of a company before you invest in it.

And this is what happened to me in the case of Raymond Realty. I was reading the Q3 earnings call transcript, and my instincts said — this right here, is a good business run by a SOLID management, available at a really good price.

What stood out to me?

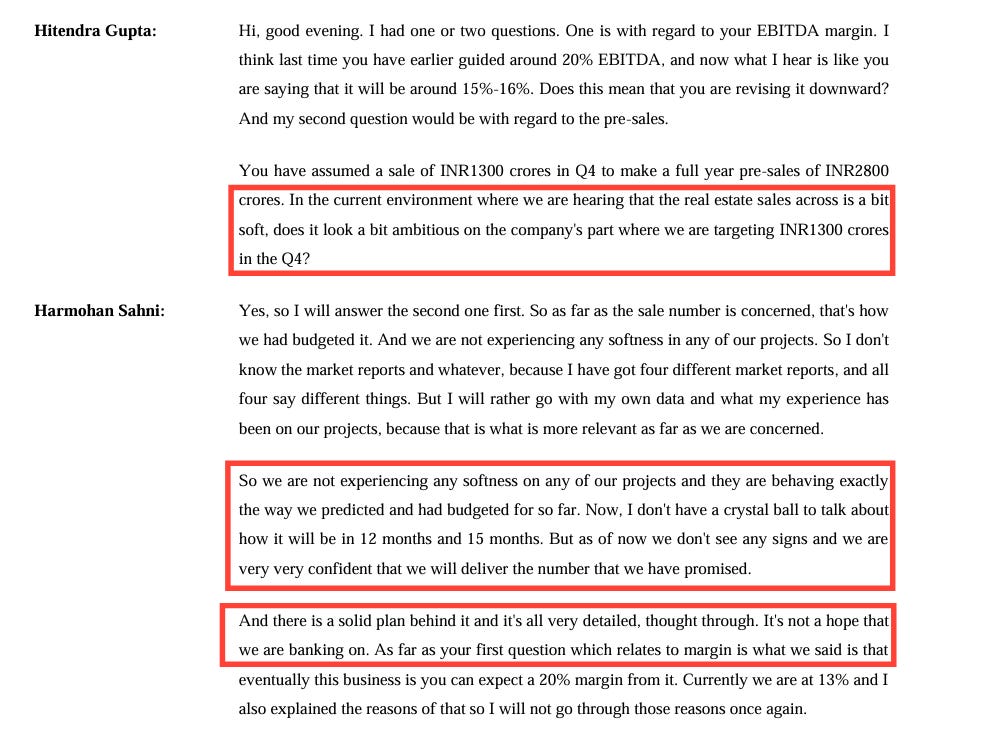

Here is an extract of the Q3 earnings call transcript, which was a clear signal about the solidity of the management.

I ABSOLUTELY loved this answer. Here’s how my mind perceived the above conversation:

Analyst: Do you really think you’d be able to achieve the pre-sales target of INR 2,800 Cr. You have achieved only INR 1,500 in the first 9 months and you’re saying you will do INR 1,300 Cr in Q4? In 3 months, you will match what you did in 9 months? Looks a little ambitious to me mate!

Mr. Harmohan Sahni: Bro, we are not joking around with our estimates. When we say we will achieve a pre-sales of INR 1,300 Cr in Q4, it means it is going to happen. We are in control of the business. We know our projections. And to be honest, I am a little annoyed that you are so surprised that we can achieve it.

For those who aren’t aware of the terminology, pre-sales refer to bookings — it is the advance home buyers pay before construction is completed and occupancy certificate (OC) is received.

My internal calculator released a verdict within seconds → The management is solid. Margins look decent. Growth drivers are in place. The cumulative future PAT > market capitalization. The stock looks cheap. Looks like a compelling buy and a wealth compounder.

Did the management walk the talk?

What the management has projected → achieving pre-sales of INR 2,800 in FY26, with Q4 pre-sales of INR 1,300 Cr. EBITDA to settle around 15-16% for FY26. Revenue & pre-sales growth of minimum 20%.

What the management achieved → pre-sales of INR 3,023 Cr in FY26, with Q4 pre-sales of INR 1,519 Cr. EBITDA of 16.3% for FY26. Revenue growth of 29% YoY.

The management absolutely smashed their own forecast, and this is partly the reason why the stock is UP around 50% in the last 2 months. And despite the surge, the stock is trading at a P/E of 12 times, which is relatively cheap.

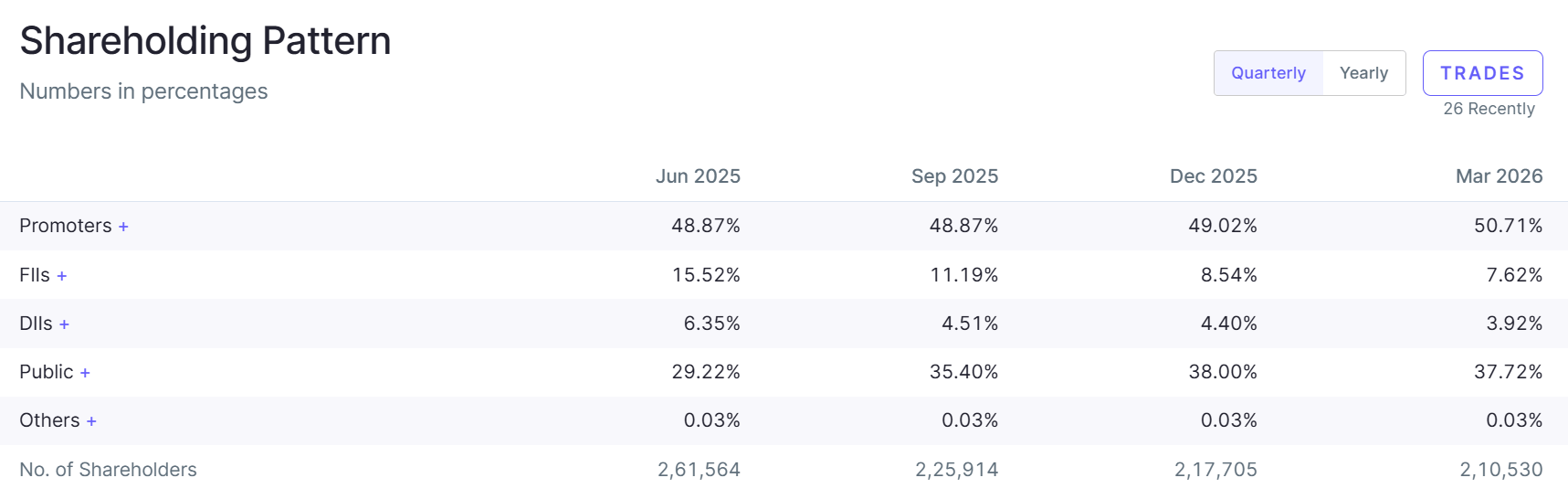

Promoters have consistently increased their shareholding for the past 3Qs, which means they’re seeing future growth in the company. An important green flag.

Business Update - Owned Projects (Thane)

The company received complete OC for TenX Habitat — RRL’s first project in Thane with 3,100 flats. This residential project was almost sold out, signifying strong buyer interest.

RRL launched two new projects in Thane in Q4 — TenX District 9 and Park Street. TenX District 9 is a residential project with 1100+ 2BHK flats. Park Street is a retail development which will host designer boutiques, cafes & iconic brands.

The company has earmarked an area for commercial real estate and will activate it when the time is right. Something to watch out for, as investors.

Business Update - JDA Projects

JDA projects contributed 54% of pre-sales booking for FY26. The management had originally communicated to achieve a 50/50 mix between JDA projects and Owned projects by FY27 — and achieved this milestone ONE YEAR in advance!

This is an asset light model, where the company enters into a Joint Development Agreement (JDA) with landowners and revenue is shared between RRL and landowners. RRL doesn’t have to buy land — which is capital intensive and quite difficult, given how scarce land is in Mumbai.

(1) RRL’s JDA portfolio comprises of 7 projects with a combined revenue potential of INR 17,000 Cr [out of which RRL’s share might be 60-70%]

(2) The company launched two new JDA projects in Q4 — Address by GS [Wadala] and Address by GS [Sion], with a revenue potential (GDV) of INR 6,400 Cr.

(3) Over the next 12-15 months, RRL plans to launch two more projects in Mahim, and both the projects are in advanced stages of approval.

(4) Added one more JDA project in Kandivali with a GDV of INR 3,000 Cr with expected launch in FY28. RRL’s revenue share is 70% with an EBITDA margin of 20-22%.

Outlook for FY27 & beyond

Management has guided for a minimum 20% growth in pre-sales and revenue every year. Expecting EBITDA margin between 16-18% on a blended basis for FY27.

The management clarified that they DON’T enter any JDA with an EBITDA of less than 20%. So, they’re not chasing growth at all costs. They are financially disciplined maintaining a D/E of 0.6 times.

From a cash flow point of view, the company will be cash flow negative at-least for the next two years as the company invests in growing the portfolio. However, the company is generating decent internal accruals, keeping debt levels in check.

When asked about the impact of the Iran-US war — the management replied that if the war drags on, input costs might increase by 3-4%, however it will be a direct pass on to the end customer and the management doesn’t expect any impact on EBITDA. This signals pricing power.

The company’s land bank in Thane is in a prime location. The average property rate in Thane is in the range of INR 11,000 - INR 25,000 per sqft. RRL operates in the INR 23,000 - INR 25,000 sqft and is at the very top of the food chain.

Conclusion

I see a LOT of potential in this company, and I like the swagger of the MD & CEO — Mr. Harmohan Sahni. He is leading from the front. They are crushing their forecasts. And the company is still available at cheap valuations.

That’s a potent mix.

Obviously, in real estate a lot of things can go wrong. One stuck project, and the return metrics go for a toss. Cash flow becomes a problem. Debt can pile on. Reputation can take a hit. So, swagger aside, the management needs to consistently maintain the same level of operational efficiency.

If they can, I see no reason why this stock shouldn’t compound shareholder wealth over the years to come.

Disclaimer: RRL is <1% of my portfolio, and I will keep adding to my position over the next few quarters.

If you liked this article, share it in your investing network. Comment, like, show some love! I spend a lot of time in research & it would mean the world to me if you could recommend this blog to your friends.

[Note: The author is not a SEBI registered investment advisor, and the contents of this article do NOT constitute investment advice. Always do your own research before you invest in a company]